Puede que los emergentes sea el nuevo destino de los inversores globales…Su evolución es muy cambiante, y venimos de unos años, desde 2009, que no han dado mucho. Correlacionan muy poco los emergentes con los mercados desarrollados. Según Bloomberg:

We're at the beginning of a turning point in the cycle where this asset class outperforms U.S. shares.

Emerging-market stocks are quietly having a huge year. Through mid-September the iShares MSCI Emerging Markets ETF, known as EEM, is up more than 31 percent, outpacing gains in both U.S. and foreign developed markets, which are up 13 percent and 19 percent, respectively.

If you’ve been a long-term holder in emerging markets, this year’s gains have felt like they were a long time coming. Total returns in EEM from 2008 to 2016 were minus 16 percent. In that same time, the S&P 500 was up almost 85 percent. Before rallying double digits in 2016, emerging-market stocks were in negative territory in four out of five years beginning in 2011.

Looking a little further back, you can see the MSCI Emerging Markets Index is currently in a lost decade in terms of price performance:

The index still is about 17 percent below its peak in the fall of 2007. Emerging markets remain an attractive asset class because of their relatively higher growth prospects compared with developed markets, but investors have to understand how things generally work in developing countries before investing.

Here are some tips to better understand this market:

Emerging markets are highly volatile. Going back to the inception of the MSCI EM Index in 1988, 76 percent of all annual calendar returns have been double-digit gains or losses. Also, almost half of all annual returns in that time were either gains or losses in excess of 20 percent. In that same period, the volatility of emerging-market stocks has been double that of their U.S. counterparts. Investing in emerging markets requires sitting through bone-crushing volatility most of the time, with higher highs and lower lows than more mature markets.

Even 10 years isn’t long-term in the stock market. Stocks generally become less risky the further you lengthen your time horizon as an investor, but even 10 years isn’t enough time to completely wipe out risk. The U.S. has experienced its own lost decades in the past, most recently from 2000 through 2009, when the S&P 500 lost 9 percent in total. Emerging markets experienced another lost decade from 1994 through 2003, when the MSCI EM Index was up just 1 percent over that 10-year stretch. Long-term in stocks is far longer than most investors assume.

Diversification matters. When the S&P had its lost decade, from 2000 through 2009, emerging-market stocks were up more than 160 percent. When EM had its lost decade, from 1994 through 2003, the S&P was up almost 185 percent. From 1988 through 2016, the returns in emerging market and U.S. stocks were almost identical, as both gave investors gains of slightly more than 10 percent per year. But if you were to construct a portfolio consisting of 80 percent in U.S. stocks and 20 percent in EM, rebalanced annually, the combined return was higher than both of the individual markets, coming in at closer to 11 percent annually.

The reason for this is that these markets show relative cyclicality with one another. This table shows how stark these cycles can be:

Using two volatile assets that both earn similar long-term returns, but take a much different path to get them, can add value to a portfolio, assuming you have the patience and discipline to stick with it when one of them is not working.

Picking the best emerging-market countries to invest in is not easy. Emerging markets are made up of vastly different countries. This has caused some to question whether they should even be considered an asset class in the first place. The problem is that the winners vary from year-to-year by such a dramatic amount that it’s very difficult to pick the winners. This table from Dimensional Fund Advisors shows the ranks of the annual performance by country over the past 20 years:

The average annual performance of the cellar dwellers was minus 26 percent, while the average annual performance of the top performers was plus 81 percent. That means the difference between the best- and worst-performing countries was more than 100 percent each year, on average. There’s no rhyme or reason to the order of these countries. So if you plan on placing a more concentrated bet on certain countries or regions you need even more intestinal fortitude than you would investing in a broad basket of emerging-market stocks, because the volatility is even higher in the individual countries.

U.S. stocks have had a great run since the financial crisis ended in 2009. Emerging markets have badly lagged in that time. One year does not make for a trend, but valuations and performance momentum could put more attention on developing-market stocks and attract flows to the sector. If that were to happen, there’s a good chance we’re at the beginning of a turning point in the cycle that could see emerging-market stocks outperform U.S. shares for years to come.

Abrazos,

PD1: Cuando se agotan las ideas y los mercados Occidentales están muy caros, aparece el mantra de invertir en emergentes…

Emerging Markets in the Digital Age

My colleagues and I have been actively speaking about the evolution taking place in many emerging markets over the past few decades. We’ve seen dramatic shifts occurring, with the often one-dimensional economic models of the past giving way to new and diverse growth drivers. This evolution includes the rapid embrace of new technologies and the rapid digitalization of economies. Here, Carlos Hardenberg, senior vice president and managing director at Templeton Emerging Markets Group, further addresses the topic.

Looking at emerging-market economies as a whole, we’ve seen a dramatic transformation from the models of the past, which were often based on commodity exports. We’ve seen a new generation of highly innovative companies located in emerging markets moving into higher value-added production processes and services. We think it’s a very exciting time for investors in this space.

The technology sector in emerging markets is providing us with many interesting opportunities—from hardware to software to various forms of e-commerce and entertainment.

Autonomous driving is an example of the growing clout of emerging-market companies. Many producers of the components and infrastructure to make autonomous driving a reality are located in emerging markets, particularly in Asia. And, they are highly specialized. For example, sensors, cameras, other lightweight components and software to enable autonomous driving are oftentimes produced in emerging markets.

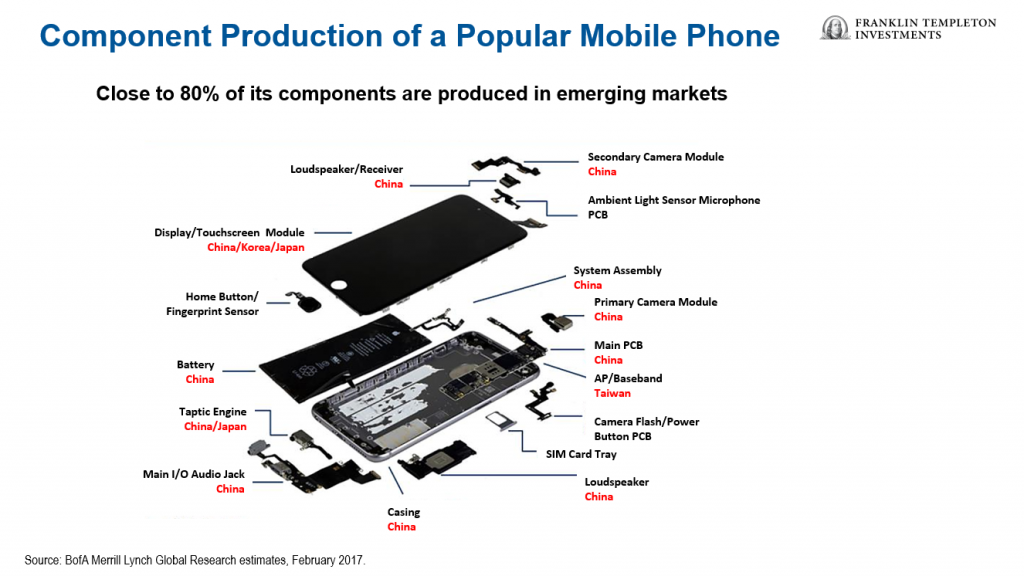

Another example is in mobile-phone technology. Some 80% of the components of one popular mobile phone are made in emerging markets, from the battery to the camera to the casing (see image below).

We know how technology has touched nearly every aspect of our lives. It has transformed how we communicate with each other, how we shop, work and play. This is true for consumers across the globe, even in what one might consider the least-developed economies. It has been estimated that 40-50% of the world’s population has access to the internet, and 70% of youth aged 15-24 use it.1It wasn’t all that long ago that no one did.

The number of internet users has increased tenfold from 1999 to 2013. The first billion was reached in 2005, the second billion in 2010 and the third billion in 2014.2 When looking at the amount of internet users globally, China (21%) and India (14%) have the largest share, above the United States (9%), Japan (3%) and Germany (2%).3

China’s “Internet Plus” strategy, unveiled in 2015, demonstrates the key role the government hopes online businesses will play in fueling its next stage of economic growth. The strategy aims to increase digitalization across the economy and to increase the presence of China’s internet-based businesses globally.

Many members of this new generation of “digitalized” consumers (including those in emerging markets) have probably never visited a physical bank branch, have never used a telephone tethered to a cord and are increasingly shunning brick-and-mortar stores to buy clothes and other wares online.

This increasing internet access means increasing opportunities. Take Indonesia, for example. Research from the International Telecommunications Union has found for each 1% increase in the internet penetration rate, unemployment growth would be reduced by 8.61%.4 The entire effect of broadband on unemployment is a combination of new jobs and existing jobs saved that otherwise would have contributed to the unemployment rate.5

In turn, consumers have more discretionary income, and the middle class is able to gain more clout. This increased spending power has driven a more consumer-oriented culture, and new and more diverse investment opportunities.

According to McKinsey research, if Indonesia fully embraces digitization, it can realize an estimated USD $150 billion in growth—10% of GDP—by 2025.6 Harnessing digital technology can boost productivity and expand economic participation across the economy. While e-commerce is growing rapidly in Indonesia—one of the world’s 10 largest economies by purchasing power parity—there is still room for more progress.

{kind=link}

{kind=link}

{kind=link}

In 2013, the Pew Research Center surveyed nearly 40,000 people in 39 countries and asked the question: Will children in your country be better off than their parents?7 Interestingly, in most of the advanced economies, the answer to the question was overwhelmingly “no.” Two-thirds of people surveyed in the United States answered that way, and the people in Britain weren’t much more optimistic their children would be better off than them, either.8

In contrast, in China, 82% of those surveyed expected their children to do better, and in Brazil, 79% felt that way.9 In Chile, Malaysia, Venezuela, Indonesia, the Philippines, Nigeria, Ghana and Kenya, the majority of people surveyed also believed that the next generation will be better off than the current one.

A Changing Profile

Not only have consumers changed, the profile of what one might think of as an emerging-market company has as well. In the past, these businesses were generally fairly simple, nascent business models. They were highly geared towards infrastructure.

During the last 10 years or so, we’ve seen a gradual migration to increasingly sophisticated business models. Emerging-market companies have established their own brand names, their own niches and have expanded beyond their home countries or region, often by acquisition.

We are seeing a new generation of emerging-market companies develop. By and large, emerging-market companies have also seen healthy cash-flow generation and improving earnings. In the past, there were certain periods where corporate balance sheets were under severe stress due to foreign-exchange debt. They ran into problems, particularly when the local currency came under pressure.

Today, these currency issues seem to be managed much better and corporate balance sheets appear to be much healthier. In general, emerging-market companies have deleveraged over time; they have cleaned up their balance sheets and repaired their business models.

It’s Still about Growth

One characteristic that has generally defined emerging markets in the past—and still does—is their high growth rate. Emerging-market economies have been growing significantly faster than developed-market economies, and we anticipate this trend should likely continue.

Despite this higher rate of growth, valuations generally appear much more reasonable than in developed markets. You can invest in many of these companies at a price that is a significant discount to what you would have to pay to invest in an equivalent business in the developed world.

Business models in emerging markets have become far more sophisticated and robust than they ever were in the past. We are very excited about the opportunities we’re finding in emerging markets today and the potential for the future.

PD2: El año pasado hicimos mi mujer y yo un curso de la Academia de Familias (https://academiadefamilias.es) sobre adolescentes. Este año nos vamos a apuntar a otro curso, dado el gran interés del primero y lo mucho que nos sirvió (tenemos dos adolescentes en casa y necesitamos muchas ideas!!!).

Te copio los cursos que organizan por si te animas a apuntarte con nosotros. Es un sesión mensual por la tarde/noche, y llevamos un plato cada matrimonio para cenar luego juntos, y comentar las dudas que surjan.

Razones para participar:

Muchos piensan que la educación sale sola, y te aseguro que no. Nosotros, que tenemos 9 hijos, nos hemos formado primero para poder trasmitirles, a nuestros hijos, una educación en valores que complemente la que reciben en el colegio, que es fundamentalmente académica, y que les sirva para estar preparados a enfrentarse a la sociedad y sus nuevas costumbres… Hay mucho que aprender y muchos son los errores que cometemos los padres por ignorancia.

Si quieres apuntarte, mándame un email y hablamos, todo por el bien de nuestros hijos y de la paz familiar.