Los mercados siguen sin inmutarse a pesar de las dudas. El Bitcoin ha explotado y se ha venido abajo, al menos algo de sensatez, pero el resto muy poco. Ligero repunte de rentabilidades, bajadas de precio de la renta fija, de la que los Investment Grade y High Yield ni se enteran…, y las bolsas, que han tenido un comportamiento parabólico, no se van a la “media”, no revierten al centro del canal, como deberían…

No mires el RSI que alucinas. ¿Revertirá a la media o se irá al 100%? Es tan ridículo…

Y el SP500 lo mismo:

Parabólico!!! ¿Se irá a la media? I bet you so…

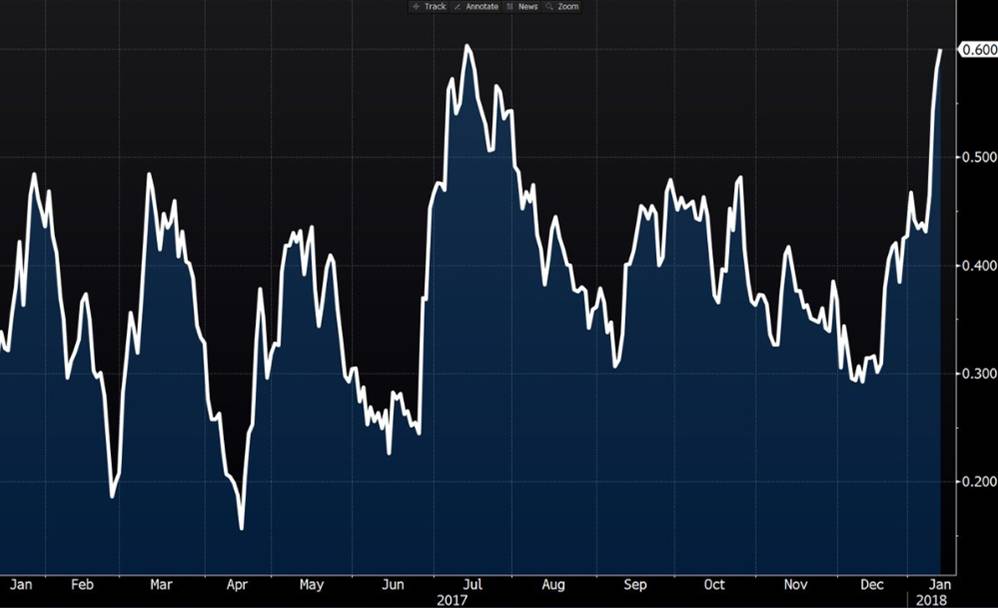

Y el euro muy fuerte, el dólar muy flojo:

Es lo que quieren para corregir el desequilibrio comercial yanqui. ¿Pero y Europa, es esto lo que necesita Alemania? Lo dudo…

EEUU:

Y los bonos, más bajos los de la periferia europea a los yanquis. Ridículo!!!

Bonos griegos versus bonos estadounidenses a dos años:

De puta coña!

Aunque ha habido un gran matiz, mira el bono a 10 años alemán:

¿Se ha acabado el chollo de tipos bajos?

¡Son los FAANG idiota! Siguen de moda, y las modas no hay quien las combata… Mueren, pero duran lo que quieren… Aunque se acaban, que se lo pregunten a Inditex que lleva 3 años muerta…

Valuing Uncertainties

As we enter 2018, numerous uncertainties are dominating the minds of American citizens and investors. We are happy to weigh in on what we consider to be both un-useful and useful uncertainties as they pertain to long duration ownership of common stocks.

Uncertainty One: Disruption

When you are ten years into an era where growth stocks have outperformed value stocks, stock promoters turn from fundamentals to futuristic fantasies.

No set of fantasies have been more effective in the last two years in the U.S. stock market than those surrounding disruption. Amazon (AMZN) is disrupting retail, pharmacy, groceries and the media business. Netflix is disrupting the media business. Tesla (TSLA) is disrupting the auto industry. Facebook (FB) is disrupting the media/advertising business and Google (GOOGL) is disrupting advertising and online e-commerce.

Follow the logic of individual and professional investors. Growth stocks have been great and the best growth stocks have been the FAANG stocks.1 The FAANG stocks have been major disruptors. Therefore, look to invest in companies which want to disrupt an industry while paying up for them through highly elevated price-to-earnings (P/E) ratios!

The effect of this has resulted in the very high P/E ratio for the Russell 1000 Growth Index. This is a valuable uncertainty.

Uncertainty Two: Human Obsolescence

A growing concern among parents is that computers and robots are going to strip employment opportunities for a large swath of young Americans. From a humorous standpoint, tech leaders are advertising a world where you would never leave your home and play golf in virtual reality, get your food delivered by drones and have a robot clean your house regularly.

The economic history of America is the shift in how we made our living. In 1900, 45% of Americans were employed in agriculture. By 1970, it was 2%. Agricultural employment was replaced by the industrial revolution. Manufacturing struggled in the inflationary 1970s. By the 1980s, manufacturing was going through a painful reduction, then financial services and information technology employment took its place.

Therefore, skeptics are underestimating the rejuvenating nature of free market capitalism and the worriers should focus on not getting in the way of capitalism. This is a nonvaluable uncertainty.

Uncertainty Three: FAANG Economic Dominance

Rarely have Americans given up control of their personal life and privacy to companies like they have with Facebook, Amazon, Apple (AAPL) and Google. Facebook knows everything about you, your relatives, your friends and what you are doing. Folks are allowing Amazon to know where they are, what they are buying and eliminating the need for human interaction.

For above-average-income Americans, Apple has created a network of people who completely depend on them for all their technology needs. Lastly, via their searches, Google knows more about you than your spouse and uses their algorithms to inhibit fair competition by guiding search results to their favored vendor. Many times, their favored vendor is themselves.

NYU Business Professor, Scott Galloway, explains the threat to our capitalistic system by channeling President Theodore Roosevelt:2

Should we break them up because they avoid taxes? Should we break them up because they destroy jobs? Galloway isn’t sold on those arguments, but instead said that Amazon, Apple, Facebook and Google should be broken up “because we’re capitalists” and that he believes the markets have failed when it comes to competition.

Galloway continues:

“Our Democracy is breaking down because these companies have become too powerful,” Galloway said. “The HQ2 thing is out of control,” he added, citing an income tax-diversion example from Chicago’s bid for the tech giant’s second headquarters. “I think our government has basically folded and said, ‘We acknowledge that you’re more powerful than us.”

The threat to fair competition these businesses pose is a valuable uncertainty.

Uncertainty Four: Expensive stocks

Both nominal and real returns from the S&P 500 Index could be disappointing the next ten years.

The chart above compares equity valuation to expected ten-year returns. Other than in late 1999 and early 2000, we haven’t had more expensive stocks in my 37 years in the investment business. This dictates low expected passive index returns. It doesn’t tell you anything about the next six months, but it speaks into a megaphone about index returns for ten years.

Combined with the popularity of passive investing, this uncertainty is valuable.

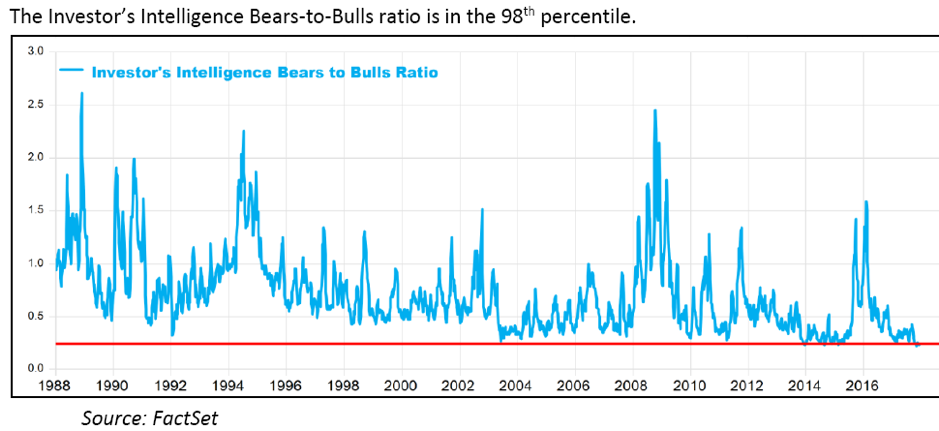

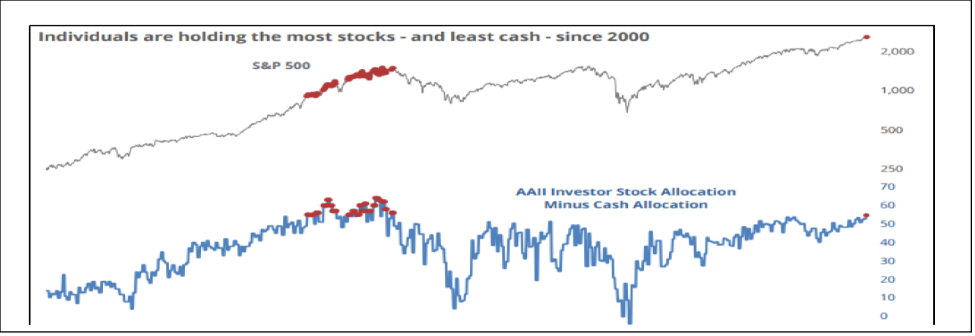

Uncertainty Five: Dangerous Psychology

At extremes, the wise investor typically does the opposite of the crowd. We stay fully invested all the time because we don’t believe in market timing. However, a great question to ask someone who runs a portfolio is how happy they would be owning shares in the next bear market. We went through the worst bear market in 80 years in 2008-2009 and the quality of the companies identified by our eight criteria is one of the things which got us through that torturous decline.

Our contrarian mind says this uncertainty is of value.

Uncertainty Six: Value Investing is Dead

A look at the history of value investing shows us that slumps in relative performance end during the next bear market in growth stocks. This happened in 1973-1974 and again in 2000-2003. The Nifty-Fifty growth stocks and the tech-bubble stocks got crushed the most in those two bear markets.3 An easy way for us to look at our most recent purchases is to ask whether we would have been excited to pay this price five years ago before the last major leg of this bull market occurred. Buying relative value in popular stock markets has been a way to beg for poor absolute performance.

The level of outperformance by growth stocks the last ten years has been fairly legendary. This could make this uncertainty extremely valuable.

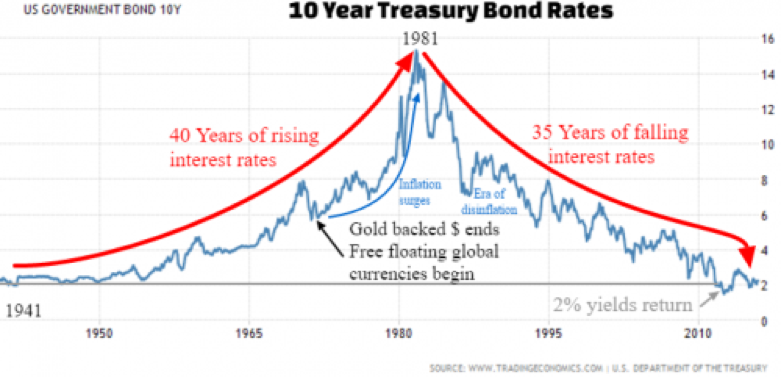

Uncertainty Seven: Rising Interest Rates

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Long duration investors should expect a mean reversion in interest rates, even though everyone who has expected this to happen looks foolish (Smead Capital Management included).

We believe the mean reversion of interest rates is a realistic and valuable uncertainty.

When you combine the un-useful and useful uncertainties as we enter 2018, we draw a few conclusions. First, never deviate from your core discipline. We are value and long duration common stock investors. We believe we are entering an era where value investors will shine in relation to the S&P 500 Index and in meeting end investor needs.

Second, dial back your risk in the areas which have been the most popular. It is hard to visualize how this plays out, but we’ll make our best attempt. Long-term bonds look like they offer a very poor risk-reward ratio. Growth stocks could continue to shine for some time and then do so poorly when their momentum breaks that everything they gain from present times — and a great deal of the money they made in the last five years — disappears.

My favorite story on this subject was in a Warren Buffett talk he did in 1996 at the University of North Carolina Business School (viewable on YouTube). Buffett had purchased 5% of Disney (DIS) in 1965 for $4 million and sold it at a 50% gain in 1966. At the end of 1972, Disney was entrenched as one of the most popular of the Nifty-Fifty growth stocks. In the 1973-1974 bear market, Disney lost 80% of its value and went all the way down to where Buffett bought it in 1965. If we ever meet him we’d like to ask him why he didn’t buy any Disney shares in late 1974.

Third, emphasize lower P/E and low price-to-free cash flow investments which are especially undervalued because of uninterrupted favor for the disruptors. We call it buying misery. This includes meritorious companies in retail, pharmacy, groceries and in old media. We like Target and Nordstrom (JWN) in retail, Walgreens and AmerisourceBergen (ABC) in pharmacy, Target and Kroger in groceries, and Discovery Communications and Tegna (TGNA) in old media.

Lastly, we believe passive indexes which are over-represented in glamour tech and momentum stocks should be avoided. It won’t matter that they represent inexpensive ownership of common stocks, because the success of momentum and FAANG stocks has reduced their natural diversification. Tech is around 27% of the S&P 500 (if you include Amazon and Netflix) which rivals the 29% stake the index had in 1999 at the end of the year.

In conclusion, there are valuable and nonvaluable uncertainties as we enter 2018. As always, we appreciate the trust and confidence shown in us by our investors. We will continue to practice our long duration stock-picking discipline to attempt to overcome whatever uncertainties prove valuable.

1FAANG stocks: Facebook, Apple, Amazon, Netflix and Google parent Alphabet

2Source: Geekwire “Professor who predicted Whole Foods acquisition: Break up Amazon, Apple, Facebook and Google” November 30, 2017.

3Nifty Fifty refers to the 50 popular large-cap stocks on the New York Stock Exchange in the 1960s and 1970s that were widely regarded as solid buy and hold growth stocks.

Abrazos,

PD1: Nos lo iban a contar, y se ha roto el cartel…

¡Qué pena! Pero ya te lo digo yo, no está en el consumo, está en el amor, a Dios, al prójimo y a uno mismo…