¿Habrá afectado la subida de volatilidad a la economía?

Desde Natixis, por Philippe Waechter:

The US economy’s worrying change of pace

Is the US economy’s current pace set to trigger major imbalances, disrupt the current cycle and spark off a significant downturn in economic activity?

The stockmarkets’ severe recent downturn reflects investors’ concerns on forthcoming trends for the global economy, and in particular the performances we can expect from the US. Firstly, they reacted to the change in stance from the Federal Reserve on forthcoming inflation trends, expected to converge towards the central bank’s target of 2% and stay there in the long term. Secondly, rising wages confirmed this idea of nominal pressure, even if the 2.9% gain announced in January’s figures was probably a result of the reduction in number of hours worked due to unusually cold weather conditions. Lastly, the handover at the Fed added another level of uncertainty. Janet Yellen did a good job of steering the US economy, will Jay Powell do the job equally well?

I have already written at length on these matters, and an article published on Forbes.fr will provide details on the uncertainties surrounding Powell’s arrival to chair the Fed. However, looking beyond these factors, a number of other questions are being raised about the US economy.

I have already written at length on these matters, and an article published on Forbes.fr will provide details on the uncertainties surrounding Powell’s arrival to chair the Fed. However, looking beyond these factors, a number of other questions are being raised about the US economy.

The first question involves economic policy and the way fiscal and monetary policies can coordinate against a backdrop of full employment. This coordination has worked pretty well so far. The US economy nosedived in 2009 and both policy areas instantly loosened: it was vital that every effort be made to avoid a drastic chain of events that would end up creating higher unemployment and a long-term hit to the standard of living. This approach was successful and the country hit its cycle trough in the second quarter of 2009, moving into an upward phase that has lasted ever since. Monetary policy continued to accommodate, but fiscal policy became restrictive in 2011 and then converged to a sort of neutral situation to avoid hampering the economy. This policy combination drove the US into one of the longest periods of growth it has enjoyed since the Second World War: the pace of GDP growth was admittedly not as brisk as before, but it did not trigger any major imbalances, as reflected by an economy running on full employment and continued moderate inflation, remaining below the Fed’s target.

This period of slower but balanced growth is coming to an end.

The economy is growing at a steady pace and unused resources are fairly limited. Production capacity utilization rates are on the up, employment for the 25-55 age range (labor market core age group) is high, although slightly lower than before the crisis at 79% vs. 80%, while involuntary part-time work is now well below its long-term average.

Against this backdrop, the best economic policy approach is to gradually take a step back. The economy is self-sustaining, so extra impetus is not required, and it is even advisable to take steps to recover leeway so that the authorities have the wherewithal to act when economic conditions do take a downturn: the Fed’s rate hikes since December 2015 should be seen as part of this strategy, as it acted very transparently and steered its communication to ensure that investors in the US and elsewhere knew what to expect.

Against this backdrop, the best economic policy approach is to gradually take a step back. The economy is self-sustaining, so extra impetus is not required, and it is even advisable to take steps to recover leeway so that the authorities have the wherewithal to act when economic conditions do take a downturn: the Fed’s rate hikes since December 2015 should be seen as part of this strategy, as it acted very transparently and steered its communication to ensure that investors in the US and elsewhere knew what to expect.

With moves to cut back taxes and hike spending, the public deficit is set to move beyond 5% of GDP this year. Fiscal policy is taking on an expansionary dimension, while monetary policy still maintains its highly accommodative slant, so the task over the months ahead will be to coordinate these two strategies. Each provides a springboard for faster growth, but this could run into a stumbling block of an economy already running on full employment. These two policies need to be carefully steered to avoid overheating, which would swiftly debilitate the US economy. There is some leeway for unemployment to fall slightly, but room for maneuver is very limited.

We can assume that monetary policy will become more restrictive and we should expect the Fed to hike its rates at a faster pace than expected – four hikes at least this year, rather than four at most.

In an article published this weekend, The Economist outlined three reasons not to worry unduly over the US situation: it is not clear that the economy is really running on full employment, inflation is not about to take a sharp surge, and tension on the labor market as a result of the acceleration in economic activity provides benefits for workers who have not really gained from the recovery.

I only fully agree with the second point: inflation risk is indeed limited. Meanwhile, looking to the first aspect, I believe that we are close to full employment, and as regards the third point, growth has primarily benefited the highest earners: this is a usual feature of the US economy and I cannot see what aspects of the current situation are likely to change this, or at least fiscal policy will not help change it. Growth provides clear benefits for the wealthiest, who enjoy the lion’s share and this is why we should raise questions on a GDP growth target in such an unequal society.

Looking at the absence of inflation, an article in this weekend’s NY Times suggested that wage trends have changed dramatically, and this could provide some explanation. Employers prefer one-time bonuses rather than salary increases: bonuses paid out once a year are inherently flexible and do not involve a definitive commitment from the company, whereas salary increases are permanent. This new remuneration mix trend is gathering pace within companies and is changing wage-price momentum.

The question is whether this situation can persist when the economy is at full employment? The answer is probably yes, for the reasons I mentioned last week. The US economy’s value-added sharing and its declining unionization do not point to strong bargaining power for workers. However, it is reasonable to assume that a long-term drop in the jobless total below the 4% mark should lead to slightly higher wage pressure. However, this should not have a very strong impact on long-term interest rates and long-term inflation projections should not accelerate sharply. I therefore do not expect a dramatic upturn on US long-term rates.

The question is whether this situation can persist when the economy is at full employment? The answer is probably yes, for the reasons I mentioned last week. The US economy’s value-added sharing and its declining unionization do not point to strong bargaining power for workers. However, it is reasonable to assume that a long-term drop in the jobless total below the 4% mark should lead to slightly higher wage pressure. However, this should not have a very strong impact on long-term interest rates and long-term inflation projections should not accelerate sharply. I therefore do not expect a dramatic upturn on US long-term rates.

Economic policy coordination will involve tighter monetary policy and hence a further flattening of the yield curve, which will obviously be bad news for the average consumer, who will suffer from the hike in short rates but not really derive much benefit from tax cuts in the long term.

The economic equilibrium in the US is shifting dramatically as a result of fiscal policy coming out of the White House and Congress. The additional budget deficit of at least $1,100 billion over 10 years is triggering a real watershed and creating a long-lasting imbalance.

The other source of disparity is the pace of US external trade in volume terms, excluding oil. The chart below shows a sharp acceleration in this balance in the last quarter of 2017 to unrivalled levels. Over the first nine months of the year, the balance stabilized at $60 billion, and came out close to $67bn over the last three months of the year and $70bn for December alone. On an annualized basis, the deficit went from a base of $700bn to $800bn in the last quarter, which is vast and will hinder growth.

The worrying point is that the euro area’s external balance increased at the end of the year, as did China’s. In other words, the increase in imports at the root of the deterioration in the US external balance, focused on consumer goods, benefited all parties. this group of three key world trade players, the country with a deficit suffers a swift deterioration in its situation, while the other two areas enjoy an improvement.

The acceleration in US domestic demand led to an increase in demand for imports and a deterioration in its external balance, while exports did not really stage an improvement. This gives cause for concern because the upward trend in domestic demand will be further accentuated by expansionary fiscal policy: the US external position is therefore set to deteriorate further.

The current US cycle has not suffered any major imbalances, which explains its longevity. Fiscal policy implemented at a time when the economy is running on full employment is set to trigger long-lasting disparities that will set the stage for the next recession (2019/2020?) and force the US authorities (Fed) to take corrective measures, while also potentially leading to investor wariness. With the presence of China and the euro area, the US is no longer the only country controlling worldwide dynamics and current events could afford the other two areas a more leading role. The worldwide balance of power is changing and the White House does not seem to have grasped the full significance of this shift.

Abrazos,

PD1: ¿Debemos estar de nuevo optimistas o reinará el pesimismo?

DE LA COMPLACENCIA AL PESIMISMO

Ha bastado una semana de fuertes caídas en las bolsas para pasar de la complacencia al pesimismo. Las correcciones, cercanas al 10% desde los máximos en los principales índices, ponen de manifiesto que lo vivido en el último ejercicio en las bolsas estadounidenses y, en menor medida en las europeas, era anómalo. No era normal que la caída desde los máximos en el último año no llegara al 4% en el Eurostoxx y ni siquiera al 3% en el Eurostoxx. La media de los 15 últimos años había sido descenso del 10% desde el máximo dentro del año, independientemente del resultado final del ejercicio.

Episodios de volatilidad como los actuales sirven para recordar algunos principios básicos de las inversiones que tienden a olvidarse cuando las bolsas sólo suben y suben.

1. Una vez despertados de la fase de absoluta complacencia, los episodios de alta volatilidad, o de fuertes oscilaciones de las valoraciones de los activos, tenderán a ser recurrentes. Las decisiones de inversión hay que adoptarlas con un horizonte temporal determinado, sabiendo que en el futuro se repetirán movimientos bruscos de los mercados, sin que por ello haya que modificar la política de inversión en el momento en que dichas turbulencias se producen. Si se cambia el objetivo de la inversión y el perfil de riesgo cuando aparecen las curvas, quiere decir que estaban mal definidos.

2. Sólo los inversores que sean capaces de soportar los vaivenes de las valoraciones deben invertir parte de su patrimonio en activos que puedan sufrir elevados descensos en su valoración. Los objetivos de rentabilidad de las inversiones deben ser compatibles con la aceptación del riesgo asumido para obtener dichos objetivos. A mayor rentabilidad esperada, mayor riesgo asumido. Sin riesgo no hay rentabilidad.

3. En estos últimos años ha sido falazmente reiterado el argumento de que ante la falta de rentabilidad de la renta fija, las inversiones deben dirigirse hacia la renta variable. Esta conclusión sólo es válida, en parte del patrimonio, para aquellos inversores que sean conscientes de la volatilidad de la renta variable y sean capaces de aguantar las oscilaciones de las cotizaciones. De no ser así, venderán en el peor momento. Nadie debe invertir en activos con posibilidad de oscilación de su valoración más allá de la cantidad que le permita dormir tranquilo. Sobrepasar el umbral del sueño sólo lleva a vender en el peor momento. Un cero por ciento de rentabilidad es mucho mayor que un -5%. Obvio.

4. La actual política de los bancos centrales perjudica seriamente a los ahorradores e inversores más conservadores. Los tipos de interés negativos les han estado empujando hacia productos que inevitablemente tienen riesgo, sin que en muchos casos sean conscientes del riesgo que asumen hasta que se materializa. La pérdida de la casi totalidad de la inversión en varios productos "innovadores" sobre índices tan complejos como el VIX (VelocityShares Daily Inverse VIX Short-Term exchange-traded note XIV, Proshares short VIX short term future), ponen de manifiesto la minusvaloración del riesgo ante una búsqueda alocada de rentabilidad. Sorprendentemente, en la lista de los principales tenedores de estos productos fallidos se encuentran grandes bancos internacionales e incluso el fondo (endowment) de alguna de las principales universidades americanas.

(Este tema merece un próximo artículo específico).

Episodios como los vividos en las últimas jornadas ponen de manifiesto que frente a la precipitación en la toma de decisiones y la sobreactuación ante los vaivenes del mercado conviene practicar el Slow Finance. Una forma de entender las inversiones, guiada por la serenidad y el buen criterio y alejada de las prisas, de la velocidad o lo impulsivo. No dejarse llevar por la vorágine de información de los mercados. Planificar a medio y largo plazo dejando de lado el vértigo del corto. El actual momento de las bolsas no debe hacerle variar los objetivos de las inversiones, ni el perfil de riesgo. No se debe pasar de la complacencia al pesimismo.

PD2: Desde PIMCO dicen:

The U.S. economic numbers released last week preceded a slide in equities, prompting keen interest in what the data may have been signaling to markets.

While the data are noisy, and it’s risky to draw conclusions from one set of reports, we believe they may reflect some trends worth watching – chief among them rising capacity constraints and growing inflationary pressures.

Consider:

+Real productivity growth was surprisingly weak in the fourth quarter (down 0.1% from the prior quarter on a seasonally adjusted annual rate basis), and unit labor costs accelerated to 2.0% despite some moderation in real compensation growth.

+The headline ISM Manufacturing Index moderated less than expected due to slowing supplier deliveries, while the production, new orders and employment indexes each declined. Meanwhile, the prices paid index increased to the highest level since 2011.

+Labor market aggregate hours, which correlate with real economic output, declined 0.42% month-over-month in January, while average hourly earnings gained 0.3% month-over-month and rose 2.9% year-over-year – the highest rate since 2009.

Teasing out the data

These data come at a time when unemployment is below various estimates of the non-accelerating inflation rate of unemployment (NAIRU), broader measures of labor market underutilization are close to pre-crisis levels and payroll growth appears to have peaked for this cycle and is decelerating. More broadly, over the past 30 years, we’ve observed just one period when decelerating payroll growth coincided with accelerating real GDP growth: during the late-1990s productivity boom.

What is the takeaway from all of this? The U.S. is starting to look more like an economy that is in the later stages of its business cycle. Absent a pickup in productivity growth, slowing payroll growth and rising economic capacity constraints should coincide with a gradual deceleration in real economic activity and building inflationary pressures. Along these lines, the weak labor productivity report released last week may raise questions about whether and to what extent productivity will rise over the coming year in response to fiscal expansion.

Equity market behavior is mimicking historical periods of accelerating inflation, slowing growth

While a range of indicators show that U.S. economic activity accelerated in the second half of 2017, the equity market deterioration is more in line with historical behavior during periods of accelerating inflation and slowing growth. In a 2014 study1 that calculated global equity market Sharpe ratios conditioned on macroeconomic cycles, equity performance was shown to be best during periods of decelerating inflation and accelerating economic growth – the state of macroeconomic fundamentals over much of 2017. The reverse was also shown to be true.

Our own research backs this up: In an analysis of the U.S., U.K., European Union and Japan that conditioned equity market performance on our economic activity and inflation indicators, we found Sharpe ratios were generally highest when equities were held during periods of decelerating inflation, and vice versa – a pattern that held even in Japan, which has experienced a prolonged period of low inflation (the exception was the FTSE 100 in the U.K.).

Regime change?

The equity market slide began against a backdrop where our growth and inflation metrics indicate that inflation has been picking up for the past several months, while economic activity also continues to accelerate – an environment historically consistent with more muted, but still positive equity market performance in the U.S. However, could the recent equity moves reflect the possibility that last week’s data is the start of a broader inflection point? Perhaps markets are already trading on the probability that the U.S. moves into a new macroeconomic regime characterized by lower economic activity and firming inflation.

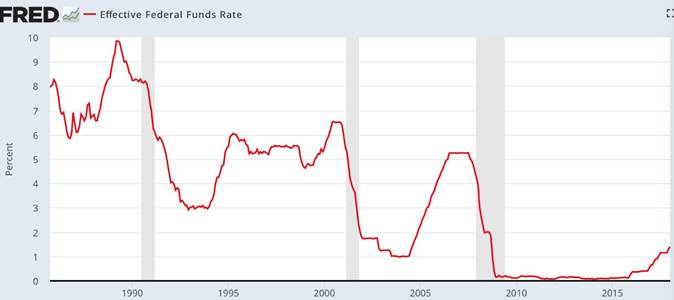

PD3: Y sí, la FED seguirá subiendo tipos de interés este año hasta que llegue su economía a una recesión. Si te fijas, siempre han sido las recesiones cuando la FED ha terminado de subir los tipos de interés:

Aunque la carga de intereses, al ser la deuda cada vez mayos, sigue subiendo y subiendo: línea roja de abajo:

Deuda de EEUU:

En porcentaje del PIB:

Déficit público de EEUU:

Y las previsiones que calcula la Oficina de Presupuestos del Congreso (CBO) para los próximos años:

O lo que es lo mismo, un trillón más de deuda por año (eso es aproximadamente lo que produce una España cada año):

Lo que le obliga al Tesoro estadounidense a tener estas emisiones nuevas, sin que compre nada la FED, y alcanzar, en breve, los 30 trillones de deuda pública:

Al que hay que añadir las deudas privadas de familias que ya alcanzan los 13 trillones de dólares:

Que a su vez, se suma al déficit externo que hay que financiar:

De ahí la necesidad de un dólar barato que tanto le gusta a Trump…, y van consiguiendo.

Si nos pasara a España, estaríamos jodidos. Bueno ya nos pasa, pero tenemos al gran mago del BCE, Mario Draghi, que nos sigue salvando hasta septiembre… ¿Luego qué?

PD4: El Señor nos mueve a usar perseverantemente la oración de petición. Ciertamente, existen otros tipos de plegaria (la adoración, la expiación, la oración de agradecimiento), pero Jesús insiste en que nosotros frecuentemos mucho la oración de petición.

¿Por qué? Muchos podrían ser los motivos: porque necesitamos la ayuda de Dios para alcanzar nuestro fin; porque expresa esperanza y amor; porque es un clamor de fe. Pero existe uno que quizá sea poco tenido en cuenta: Dios quiere que las cosas sean un poco como nosotros queremos. De este modo, nuestra petición, que es un acto libre, hace que el mundo sea como Dios quiere y algo como nosotros queremos. ¡Es maravilloso el poder de la oración!