Muchos cambios producidos en los mercados emergentes en los últimos años. Un amplio resumen:

The Metamorphosis of Emerging Markets

by Howard Schwab, Chad Cleaver, Rich Thies, Trent DeBruin, Ayman Ahmed of Driehaus Capital Management

The relative performance of emerging markets has been unremarkable over the past decade, however meaningful changes have taken place in the fundamental and financial construct of the asset class that are relevant for asset allocators. Most notably, the composition of the index has seen dramatic shifts in sector, country, and stock constituents, reflecting an underappreciated transition in the fundamental forces increasingly driving developing market economies. Rising consumerism and growing everyday use of technology within the developing world represent meaningful fundamental changes in economic behavior and such thematics are accessible through a growing number of listed corporates and globally competitive companies.

Additionally, prudent macroeconomic policy implementation and selective structural reforms have laid the foundation for more stable and sustainable long-term economic growth, while companies are being managed in a more efficient and shareholder-friendly manner. With longer-term valuation metrics remaining attractive for many developing equities on a comparative basis, the significant changes to the emerging markets asset class are increasingly important to consider. Because we feel that some of these shifts in the emerging markets story may be underappreciated or misunderstood, in this piece we present views from various team members pertaining to the changing face of emerging markets.

The Opportunity Set is Improving

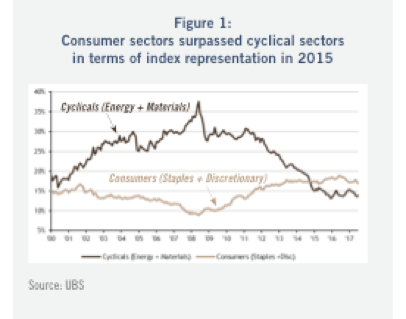

Over much of the past thirty years, the emerging markets asset class has frequently been regarded as something to “rent” as opposed to own for most investors. Known for commodity-reliant economies and cheap sources of manufacturing labor, developing nations’ financial markets historically gyrated around the ebbs and flows of global economic activity. While this phenomenon has not entirely vanished, the composition and macro sensitivity of emerging market equities have nonetheless been shifting. Part of this transition can be explained by the fading omnipotence of globalized trade as well as a somewhat related policy-driven emphasis on spawning more domestically-oriented economies. Developing countries’ demographics position them well to pivot in this direction and unsurprisingly, the evolution of the asset class has reflected this reality (Figure 1), with consumer-related equities now composing a greater percentage of the MSCI Emerging Markets Index than cyclicals.

While the steady ascent in developing market consumerism has been materializing for nearly a decade, the more recent quantum leap in technological innovation and adoption in emerging markets has been surprisingly abrupt. China illustrates a prime example of this development, with industries such as shopping centers completely marginalized by e-commerce behemoths Alibaba, Tencent and JD.com. These platforms are revolutionizing consumer, merchant, and advertiser behavior through digital ecosystems and are increasingly proving to be globally competitive (yes, even against the likes of Google and Facebook) in areas such as artificial intelligence, e-payments, and logistics. China has similar long-term aspirations in other areas including healthcare.

Alongside the changing fundamental landscape of the developing world, the financial framework is evolving as well. Brazil, for example, has introduced the Novo Mercado market index that sets out more stringent listing rules defined as:

“Good corporate governance practices, more stringent than those present in the Brazilian legislation. These rules, consolidated in the Listing Rules of the Novo Mercado, expand shareholder rights, improve the quality of information usually provided by companies and widespread ownership, and determine the resolution of corporate conflicts by a Board of Arbitration that offer investors the security of an alternative more responsive and specialized.” (Source: BM&F Bovespa)

In another example, China has recently enacted steps to increase access between mainland China (known as A-Shares) and Hong Kong (which provides a platform for global investment money) financial markets. The program, known as “Stock Connect” aims to improve mutual market access as part of a strategic plan targeted at deepening and broadening the accessibility of Chinese equities, and ultimately bonds as well. The launch of the connect program involved various operational and legal issues including T+0 trade settlement, payment, delivery, and the creation of trade accounting structures. Thus far, the connect program has proven successful and represents an incremental step toward greater integration into the global financial system for China.

India represents a third example of financial market progress with its encouragement of a domestic investment culture. Through a series of reform-oriented measures, Indian household equity holdings as a percentage of savings have risen from 2.2% in 2014 to approximately 4.0% today and net monthly domestic inflows continue to trend higher (Figure 3). Establishing a stronger domestic equity base is important for the development of developing financial markets and a number of emerging countries are already targeting similar measures.

Developing nations represent approximately 40% of global GDP and accounted for 80% of global GDP growth in the latest twelve months, yet they represent only 10% of global equity market capitalization (Figure 4). As these economies increasingly generate growth via areas like technology, education, healthcare, and consumer services, the configuration and behavior of the underlying asset class will similarly shift. Returns on capital should gradually converge towards developed market levels, capital expenditure (CAPEX) and asset intensity should reduce, return dispersion within the index should expand, and earnings volatility relative to history should diminish.

An example of this metamorphosis can be seen in the Chinese education space - an industry poised to grow 8% annually to $140 billion by 2020 (source: Frost & Sullivan) - where leading companies such as a large education company should deliver a 40% earnings per share compound annual growth rate between 2017-2020 while achieving return on equity (ROE) of nearly 40% with consistently positive free cash flow. These realities reinforce the notion that relative to history, heavyweights in the emerging markets will increasingly be companies that investors can “own” rather than “rent” while providing valuable portfolio diversification at the same time.

Slowly buy Surely

In recent years, several emerging market countries have undertaken structural reforms to better position for long-term sustainability. While reform can be a slow process and involve hurdles along the way, we see meaningful progress in a number of areas.

Between 2000 and 2008, China built overcapacity across a number of industries that supported the country’s urbanization phase, including steel, cement, aluminum, shipbuilding, and coal. Once a net importer of steel, China currently maintains more steel production capacity than the rest of the world combined. This debt-financed capacity overbuilding created risks for the industrial sector and the banking system in a cyclical downturn. Over the past two years, China has shut down over 10% of its steel capacity, and has begun similar supply side reforms in other areas previously plagued by overcapacity, supporting the profitability of these industries, while also reducing the associated financial sector risk.

Amid much fanfare, India’s Prime Minister Narendra Modi came into power in 2014 within a government that had previously been plagued by policy paralysis. Three years later, Modi has largely delivered on his promises, undertaking targeted stimulus, deregulation, and tax reforms that promote a formalization of the economy, while clamping down on corruption. These measures have been well received, resulting in a surge in both portfolio investment flows as well as foreign direct investment. The reforms undertaken by Modi place India on a clearer path to realizing its demographic dividend.

Brazil has taken bold action in an attempt to shore up its fiscal deficit. The country’s debt to GDP ratio rose from 55% in 2004 to around 74% today, which creates a heavy burden in a high interest rate environment. Labor reform was recently passed by Brazil’s Congress, with an aim to increase the flexibility of Brazil’s labor market, improve productivity, and create jobs. The coming months will bring about a push for pension reform, which could have a meaningful impact on the deficit, considering Brazil currently spends over 10% of GDP on pension benefits.

These three examples are just a snapshot of the reforms taking place in emerging markets, which also include energy reform, environmental protection, privatizations, and state-owned enterprise reform, among others. Alongside such macro-oriented measures, we observe emerging market corporate management teams undertaking similar initiatives to improve their efficiency and streamline their operating structures.

First, companies are showing increasing discipline and shareholder alignment with respect to their capital allocation decisions. Many companies have adapted to an environment of slower global growth by opting not to pursue top line growth at all costs, but rather to operate in a more efficient manner, cutting operating expenses and rationalizing CAPEX. Not only is the declining CAPEX intensity we have witnessed over the past several years a likely precursor to rising profit margins, but it has also resulted in increasing dividend payouts.

Additionally, several Brazilian companies have recently entered into new shareholder agreements that simplify the corporate structure, promoting better alignment with minority shareholders. This should enable these companies to migrate to the previously mentioned Novo Mercado, a segment of the Brazilian equity market for companies with strong corporate governance practices and transparency.

These shareholder friendly measures undertaken by EM corporates, along with structural reform at the macro level, point to the potential for ongoing reduction of the risk premium associated with emerging markets, as investors are likely to pay a higher multiple for the resulting visibility in the long-term growth profile.

Instability Breeding Stability

While the long-term potential of emerging markets relative to developed markets has continually remained attractive, the high levels of macro instability since 2013 led many investors to remain tactically underweight the asset class due to heightened perceived risks. Those very same risks, namely bloated external deficits, high levels of inflation, wider fiscal deficits, and steady FX depreciation have forced internal adjustments on many countries. While we acknowledge that short-term bouts of volatility remain a risk, the adjustment undertaken by numerous economies since 2013 renders the current emerging markets landscape much more stable than it has been in the past.

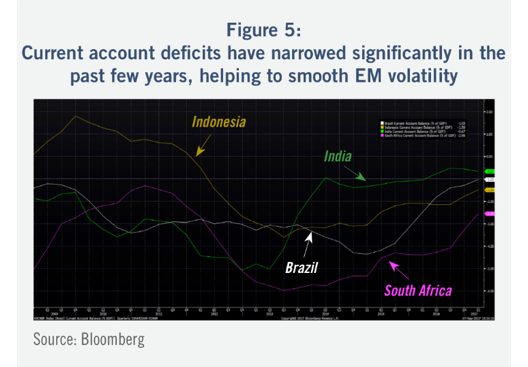

The cornerstone of this improved stability is smaller external deficits. There has been a substantial improvement in external positions, with the countries once referred to as “fragile” having exhibited marked narrowing of trade deficits over the past two years (Figure 5). Most of this external deficit reduction has come from weakness in domestic demand and thus, in imports. Exports have also been a positive contributor in recent years, helped along by pickups in manufacturing, technology, and commodities. While the export side of the equation may prove to be somewhat cyclical over time, the structurally improved ability to withstand shifts in the cycle via policy and corporate governance should ultimately enable emerging markets to chart a stronger course in the future.

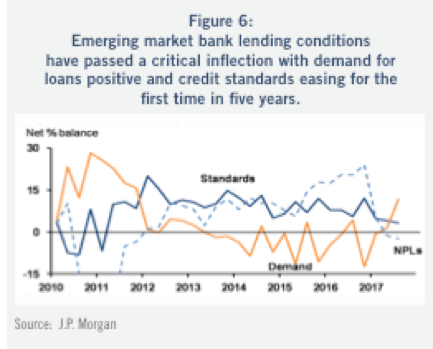

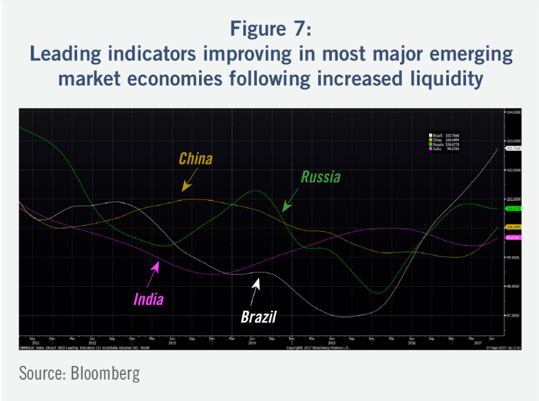

There are a few things that have been very reliable in emerging markets over the past decades. First, with much higher potential growth rates, higher real rates, and higher returns on capital, money tends to flow to emerging markets when risks decline. We have seen that very clearly this year, with flows returning to all emerging market asset classes as macro risks and the threat of FX losses have waned. Second, when financial conditions ease in emerging markets, growth actually responds. Since the global financial crisis, developed market monetary conditions have been as easy as possible, yet there has been very little growth recovery. We do not expect this to be the case in emerging markets, and rather see the economies in the very early stages of a typical cycle, where growth improves as financial conditions loosen and credit begins to grow again. (Figures 6 and 7)

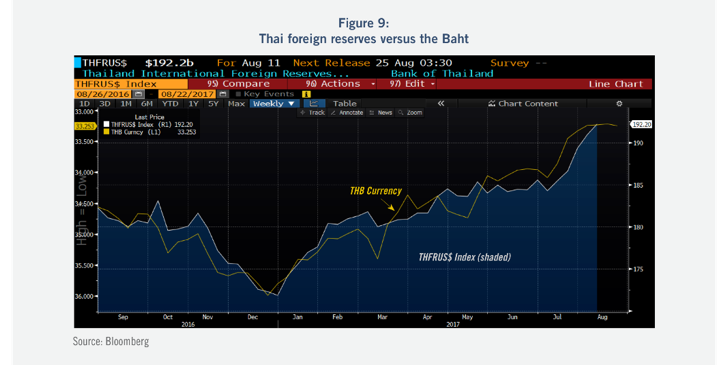

Given the improvement in external positions across emerging markets, we are not surprised to see currencies appreciating. However, this has not always been the case. In the past, due to consistent currency intervention by EM central banks (selling domestic currencies versus reserve currencies), investors were often left guessing whether improving current accounts would in fact lead to currency appreciation. Today, with widespread global trade growth and shared rhetoric against currency manipulation, the logical relationship between external balances and currencies is intact. Thailand provides a good illustration of this dynamic.

Thailand’s exports have been extremely strong (Figure 8). Simultaneously, lower oil prices are compressing imports, supporting the current account. As the current account surplus balloons, FX reserve accumulation is accelerating (Figure 9). On a real effective basis, the Thai Baht is as strong as it has been in the past fifteen years. Widening current account surpluses and appreciating currencies are consistent trends across most of the exporting nations in the Asia Pacific region. As the current account balloons and the Baht appreciates, it creates a positive feedback loop by putting further downward pressure on inflation. This is common across many of the high yielding emerging market countries, which fuels the positive carry trade.

Emerging market inflation has fallen rapidly since the middle of 2016 (Figure 10). In fact, the current level is even lower than the financial crisis trough when domestic demand was under immense pressure. With inflation falling and central banks maintaining a cautious approach, real yields have increased. In fact, emerging market real yields are at all time highs (Figure 11) which is attracting captial at record levels (Figure 12) and breeding stability across all emerging market asset classes. This stability will eventually facilitate policy rate reductions by central banks, which should support domestic demand growth and an extended positive cycle for emerging market economic growth and asset class performance.

Improving Growth and Profitability at a Reasonable Price

The past seven years have been challenging for emerging markets, both in absolute and relative terms. During this time, the MSCI Emerging Markets Index has been roughly flat in US dollar terms while the MSCI World Index has risen more than 60%. Factors such as slowing Chinese GDP growth and a global commodity down cycle weighed on emerging market earnings growth, return ratios, and valuations, while developed markets sailed through this period relatively unscathed. We see the tide now turning as emerging market fundamentals have reached a positive inflection and asset class underperformance in recent years has created strong potential for outperformance versus developed markets over the coming years.

While superior growth potential has historically been a key reason to allocate to emerging markets over developed, the former has not delivered in recent years. In fact, 2016 was the first time in five years when emerging market earnings per share grew faster than developed market earnings per share. Emerging economies have better long-term growth prospects, based on demographics and productivity improvement. With prior cyclical headwinds such as currency weakness and economic slowdown now easing, emerging markets should once again grow earnings at a faster rate than their developed market counterparts (Figure 13).

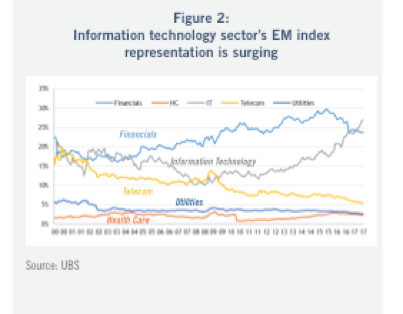

Following five consecutive years of contraction, emerging market return on equity (ROE) expanded last year. DuPont analysis reveals the key drivers of ROE compression in recent years were falling margins and asset turnover (Figure 14). Looking ahead, ROE should expand as margins and asset turnover recover, bolstered by stronger earnings growth and improving corporate management. It is worth noting that emerging market ROE is increasing relative to developed market for similar reasons. Rising emerging market ROE is even more impressive when considering that leverage is falling from peak level. While part of the uplift is being driven by recovery of the commodity cycle from a depressed level, another driver is growing representation of the high margin, information technology sector within the index. This compositional shift should ensure a structurally healthier ROE profile for the asset class.

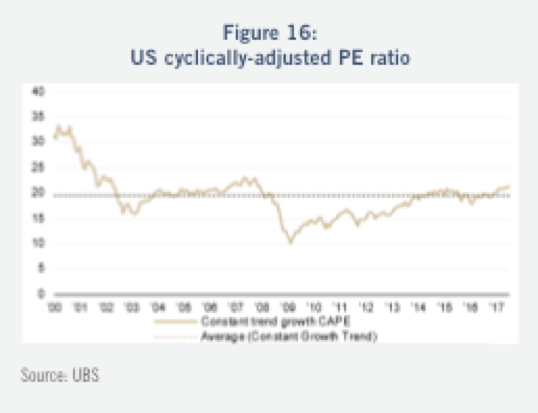

While near-term earnings multiples have rerated significantly over the past year and a half, emerging markets remain attractively valued on longer-term measures and relative to developed markets. On a cyclically-adjusted price to earnings (PE) ratio, which measures valuation on a multiple of ten-year trailing earnings, developing markets are trading near historical trough (Figure 15). Conversely, the US cyclically-adjusted PE is near the high end of its historical range, excluding the tech bubble (Figure 16). On a relative multiples basis, the discount of emerging versus developed is one standard deviation stretched versus history. Relative valuation has historically tracked relative economic growth rates for the two groups. After five years of convergence, the growth spread of emerging over developed has begun to expand once again, which should favor relative rerating of the former.

Despite strong relative performance of emerging markets since the trough in early 2016 (emerging has outperformed developed by more than 20% over this time period), investors remain under allocated to the asset class. Fund allocation data shows global fund managers with historically extreme underweights to emerging markets (Figure 17). We see strong potential for funds to flow from developed to emerging as asset allocators embrace the improving absolute and relative case.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Conclusion

Investors who have grown accustomed to the conventional view of emerging markets may be surprised to learn of the changes that have taken place over the past decade. Challenges for emerging markets during this volatile period have laid the foundation for a steadier and more sustainable fundamental future. The representation of highly cyclical industries within the index has fallen, replaced by more sustainable and compelling growth companies in areas such as technology and consumption. Progress is being made with historically elusive structural reform, while companies are being managed better. Earnings growth and returns of the asset class are improving in absolute and relative terms, while valuation looks attractive on longer-term measures and relative to developed markets. While the asset class will no doubt remain susceptible to shorter-term periods of volatility, we are excited about the multi-year outlook and believe emerging markets’ attractiveness within a global asset allocation continues to rise.

Abrazos,

PD1: Muy buenos consejos, mejor que el yoga!!!

30 útiles consejos para evitar el estrés

Sentimos que el tiempo no alcanza para nada.

Te dejamos estos sencillos consejos para ayudarte:

1. Disfruta cada día.

2. Levántate a tiempo para empezar el día sin apuros.

3. Deja un poco de tiempo extra para hacer las cosas o llegar a algún lugar.

4. Aprende a decir que no a proyectos que no pueden introducirse en tu horario de trabajo o que comprometerían tu salud mental.

5. Delega tareas a personas capaces.

6. Simplifica tu vida.

7. Recuerda que menos es más.

8. Ordena tu tiempo. Dale más tiempo a grandes cambios o proyectos difíciles.

9. Organízate de tal manera que cada cosa tenga su espacio.

10. Escribe las cosas.

11. Todos los días encuentra un momento para estar a solas contigo mismo/a y otro para estar a solas con Dios.

12. Haz suficiente ejercicio.

13. Aliméntate bien, con una dieta saludable y balanceado/a.

14. Bebe agua. Tu cuerpo se deshidrata cuando estás bajo estrés, tensión ó ansiedad. Beber agua contribuye a la relajación.

15. Haz oración.

16. Descansa lo suficiente.

17. Toma un baño relajante.

18. Camina, ponte ropa cómoda y camina un rato. Una caminata al aire libre, de 10 a 30 minutos diarios, te ayuda a relajarte.

19. Lleva contigo algo para leer mientras esperas en colas.

20. Cultiva un hobbie o afición.

21. Sonríe.

22. ¡Ríe más fuerte!

23. Desarrolla una actitud tolerante; la mayoría de las personas tratan de hacer las cosas de la mejor manera posible.

24. Habla menos, escucha más.

25. Sé amable con las personas que no lo son; tal vez ellos lo necesitan más.

26. Rodéate de recuerdos lindos, enmarca tus fotos favoritas y colócalas en un sitio visible, pon frases positivas en lugares visibles.

27. Reduce el ritmo, aprende a disfrutar cada momento de tu vida.

28. Empieza a buscar amistad con gente feliz y no estresado/a.

29. Ve a dormir en el momento preciso. Duerme mínimo 7 horas

30. Todas las noches, antes de dormir, haz un examen de conciencia y un recuento de todas las cosas buenas que tuviste en ese día. Agradece a Dios, pide perdón por tus faltas y pídele que te dé un descanso reparador