EMAIL DE MAÑANA

Alucinan…y se ve reflejado en nuestra prima de riesgo, ya está en 326 y por encima de Italia. Ya estamos de nuevo. Poco hemos durado tranquilos. MIERDA. Ay de los políticos, ay…

Rajoy ha actuado como el tipical macho hispano, y no estamos para fardar de nada… Veremos las consecuencias, me temo, funestas… Más que importarnos lo que dice la prensa local (ABC, Razón, El Mundo o El País), que nos la repanfinfla, debemos estar atentos a lo que se dice por ahí, lo que dicen los guiris. Y no es nada bueno:

Dice Steve Collins:

The Spanish rebellion has begun, sooner and more dramatically than I expected.

As many readers will already have seen, Premier Mariano Rajoy has refused point blank to comply with the austerity demands of the European Commission and the European Council (hijacked by Merkozy).

Taking what he called a "sovereign decision", he simply announced that he intends to ignore the EU deficit target of 4.4pc of GDP for this year, setting his own target of 5.8pc instead (down from 8.5pc in 2011).

In the twenty years or so that I have been following EU affairs closely, I cannot remember such a bold and open act of defiance by any state. Usually such matters are fudged. Countries stretch the line, but do not actually cross it.

As many readers will already have seen, Premier Mariano Rajoy has refused point blank to comply with the austerity demands of the European Commission and the European Council (hijacked by Merkozy).

Taking what he called a "sovereign decision", he simply announced that he intends to ignore the EU deficit target of 4.4pc of GDP for this year, setting his own target of 5.8pc instead (down from 8.5pc in 2011).

In the twenty years or so that I have been following EU affairs closely, I cannot remember such a bold and open act of defiance by any state. Usually such matters are fudged. Countries stretch the line, but do not actually cross it.

With condign symbolism, Mr Rajoy dropped his bombshell in Brussels

He is surely right to seize the initiative.Spain

There comes a point when a democracy can no longer sacrifice its citizens to please reactionary ideologues determined to impose 1930s scorched-earth policies. Ya basta.

What is striking is the wave of support for Mr Rajoy from the Spanish commentariat.

This one from Pablo Sebastián left me speechless.

My loose translation:

"Spain

"The behaviour of the European Commission towardsSpain over recent days has been infamous and exceeds their treaty powers… these Eurocrats think they are the owners and masters of Spain

"Spain and other nations in the EU are sick and tired of Chancellor Merkel's meddling and Germany 's usurpation – with the help of Sarkozy's France

"Rajoy must not retreat one inch. The stakes are high and the country is in no mood to suffer humiliations from a Chancellor who is amassing all the savings of Europe and won't listen to anybody, as if she were the absolute ruler of theUnion . Merkel and the Commission should think hard before putting their hand into the sovereignty of this country – or any other – because it will be burned."

This then is the fermenting mood in the fiercely proud and ancient nation ofSpain

As for the "Fiscal Compact", it is rendered a dead letter by Spanish actions.

Gracias a Dios. If the text were enforced, the consequences would be ruinous. It enshrines Hooverism in EU law, and imposes contractionary policies without the consent of future parliaments – including any future Bundestag. Indeed, it probably violates the German constitution.

But it won't be enforced in any meaningful sense because the political realities of the EU are already intruding, and will intrude further. A president François Hollande ofFrance

He is surely right to seize the initiative.

There comes a point when a democracy can no longer sacrifice its citizens to please reactionary ideologues determined to impose 1930s scorched-earth policies. Ya basta.

What is striking is the wave of support for Mr Rajoy from the Spanish commentariat.

This one from Pablo Sebastián left me speechless.

My loose translation:

"

"The behaviour of the European Commission towards

"

"Rajoy must not retreat one inch. The stakes are high and the country is in no mood to suffer humiliations from a Chancellor who is amassing all the savings of Europe and won't listen to anybody, as if she were the absolute ruler of the

This then is the fermenting mood in the fiercely proud and ancient nation of

As for the "Fiscal Compact", it is rendered a dead letter by Spanish actions.

Gracias a Dios. If the text were enforced, the consequences would be ruinous. It enshrines Hooverism in EU law, and imposes contractionary policies without the consent of future parliaments – including any future Bundestag. Indeed, it probably violates the German constitution.

But it won't be enforced in any meaningful sense because the political realities of the EU are already intruding, and will intrude further. A president François Hollande of

En un informe de Lombard Street dice cosas impensables o no escritas hasta ahora. Estudia la conveniencia de una salida del euro de varios países, los malos o los buenos. Si te fijas en los números para España son desastrosos. Ni conseguimos reducir nuestros desequilibrios, sino todo lo contrario, no sólo tenemos crisis para largo, sino que ésta se sigue incrementando… El informe no tiene desperdicio, léetelo:

Report Shows Netherlands

Inquiring minds are reading a 73 page detailed report The Netherlands & The Euro that explains country by country whyItaly , Greece , Portugal , and Spain are going to need lots more money, and the Netherlands and Germany

The study highlights the fundamental flaws of the Economic and Monetary Union (EMU), the damage done by the euro to date to theNetherlands Netherlands

Here are some snips from the report regarding the finances ofItaly , Spain , and Portugal

Inquiring minds are reading a 73 page detailed report The Netherlands & The Euro that explains country by country why

The study highlights the fundamental flaws of the Economic and Monetary Union (EMU), the damage done by the euro to date to the

Here are some snips from the report regarding the finances of

Italian Projections

It cannot be assumed that roll-over of existing debt as it matures can be done with private lenders, as in the past.Italy Italy Italy Italy

It cannot be assumed that roll-over of existing debt as it matures can be done with private lenders, as in the past.

{kind=link}

All of the above highlights the risk that

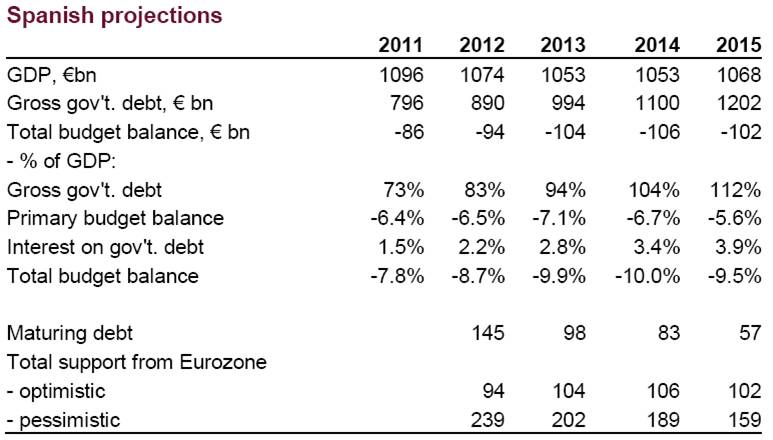

Spanish Projections

The Spanish government has actively pursued a tighter fiscal stance, in line with the current Eurozone insistence on austerity. It is likely to prove counter-productive. Unemployment has already mounted from 8% in late 2007 to over 20%. The government's GDP estimates have ceased to be credible, registering a real decline of just under 5% in the recession, with negligible recovery since. It is highly improbable that such a recession, less than that of the US, Germany or Britain, would lead to a 12 percentage-point rise in unemployment, even with the lay-off of masses of low-productivity casual construction labour, much of it migrants from eastern Europe. But, as elsewhere, denial followed by bluff has been the standard Eurozone response to critics throughout the crisis. Almost certainly, the true fall in GDP has been much greater.

The risk, obviously, is to the Spanish banking system. Even after Japan's six-year "drying-out" period, its banks had to undergo a substantial debt write-down in early 2003 (8% of GDP) before economic recovery became sound. In

In Portugal, where the chief export market is potentially recessionary Spain, where cost competitiveness is worse than Spain, and the business debt burden much higher at 16 times net cash flow, as is government debt relative to GDP, the private sector is actually still in deficit – the current-account deficit is larger than the budget deficit.

It is almost impossible to see how

In this projection of Portuguese financial needs, the assumption is that coping with the extremity of business debt ratios creates a crisis that requires the write-off of existing debt over three years, as in

Austerity + Subsidy – Not a Cure

In summary terms, curing a country's excessive debt problem requires one (or more) of the three 'de's: devaluation, default or deflation. The Eurozone has ruled out the first two – and adopting the third seems likely to achieve a fourth 'de': depression.

With unchanged Eurozone membership, the only method of adjusting costs and prices in Med-Europe to be competitive without extreme and constantly reinforced austerity, leading to depression, would be stimulation of rapid inflation in The Netherlands and Germany for a decade or two; and acceptance over that adjustment period of large fiscal subsidy payments to the deficit countries – not loans to be repaid later, but unrequited transfers. Such transfers are already happening through banking systems being subsidised by access to the ECB's repo "window" to finance themselves at interest rates well below those paid by their own governments

The danger for The Netherlands is that the potential for subsidy needed by Med-Europe is open-ended. All official scenarios are based on a rapid reversion to recovery, both in Eurozone economies and financial markets. Official scenarios never anticipate recession or financial crisis. This is part of the problem. The imbalances that are poisoning the Eurozone economies cannot be acknowledged because their cure, once they are acknowledged, clearly requires major exits from the euro, or its disbandment. Unacknowledged, they remain unaddressed, so continued financial deterioration is likely, unless the core Eurozone countries step in and provide the continuing subsidies outlined above.Aggregate Potential Costs of Current EMU Membership

{kind=link}

Y este otro, Edward Hugh, no está muy positivo tampoco, y lo malo es que le lee todo quisqui guiri, y cuando digo todo quisqui es todo quisqui:

Homeric Similes And Spanish Debt

"Nihil sapientiae odiosius acumine nimio" (Nothing is more hateful to wisdom than excessive cleverness)

Petrarch, "De Remediis utriusque Fortunae"

Petrarch, "De Remediis utriusque Fortunae"

Like Leo Messi charging his way through a packed Real Madrid defence, twisting now this way, now that, never stopping without being stopped, so did the Spanish sovereign debt surge forward, breaking directly into the red zone near the penalty box, provoking confusion and consternation amongst horrified EU officials and regulators forced to look on as it blindly sought to touch down somewhere well beyond the authorised 100% finishing line.

Now Victor quotes me on two counts: the real size of

"Spanish sovereign debt is already over 80 per cent of GDP," said Edward Hugh, a Barcelona-based economist. "I think it's getting nearer 90 per cent"......Mr Hugh also said the situation in Spain could not be compared to the confusion in the public accounts of Greece because much of the Spanish data are public and made available by the Bank of Spain, or can be deduced from official sources. But he added that the centre-right government's transparency risked curbing Spain

Well, while it's the first claim that is controversial and in need of justification (and believe me Victor Mallet demanded to see the justification for the numbers before putting up the quote) let's start with the second one first as it forms an important part of the background. I think it is very important to understand that Spain is not Greece Spains

Similarly in the case of the public administration, auditors and controllers are in place to constantly measure and follow the exectution of the annual budget at all levels, but again what they know is often one thing, and what they actually say is another. WhenSpain

Let me take another example, from an area outside the financial system and public finance: migration statistics. Between 2000 and 2008 around 6 million irregular migrants arrived inSpain

Similarly in the case of the public administration, auditors and controllers are in place to constantly measure and follow the exectution of the annual budget at all levels, but again what they know is often one thing, and what they actually say is another. When

Let me take another example, from an area outside the financial system and public finance: migration statistics. Between 2000 and 2008 around 6 million irregular migrants arrived in

{kind=link}

We know with some degree of accuracy the number of such migrants present (although not authorised to be) in Spain Spain

Well, you may say, that is fine, but how do we know the register doesn't overstate the number of migrants? In fact, at one point it did, since migrants were only obliged to confirm their continuing presence every two years. That was when the focus was on who was coming in, but since the economic crash and the massive surge in unemployment, for a variety of reasons the emphasis has moved to who is still here. So the interval for address confirmations and things like that has changed, and most of those who don't have residence rights are now required to confirm their presence every few months, which means that Spain has some of the most accurate data on migrant flows to be found within the confines of the EU (and possibly anywhere).

Well, you may say, that is fine, but how do we know the register doesn't overstate the number of migrants? In fact, at one point it did, since migrants were only obliged to confirm their continuing presence every two years. That was when the focus was on who was coming in, but since the economic crash and the massive surge in unemployment, for a variety of reasons the emphasis has moved to who is still here. So the interval for address confirmations and things like that has changed, and most of those who don't have residence rights are now required to confirm their presence every few months, which means that Spain has some of the most accurate data on migrant flows to be found within the confines of the EU (and possibly anywhere).

{kind=link}

Now, you might say, why be so meticulous in collecting all this information, why not follow the UK Spain and not the UK (or Greece ) and this is the point of the present rigmarole, to give an idea of how things work in Spain

Now, on the public accounts issue, I actually started digging into all this in the summer of 2010, and indeed posted an interim "report" at the time. So it is something of a mystery to me why all the hedge funds, journalists and bank analysts have taken so long in waking up to "Spain's regional debt problem", especially since all the information on the topic is freely available on the Bank of Spain website. It seems to me, that people see what they want to see at any given point in time, and this is the point of the Petrarch quote which starts this post. It comes from an Edgar Allen Poe short story, the purloined letter, and to cut a long issue short, a letter goes missing which no one can find, and the reason they cannot find it is precisely because it is lying their before them, on the living room mantelpiece.

If you try to go rummaging round for Goldman Sachs style interest rate swaps inSpain Spain

But before we did down any deeper, just to let us all see where we are, why don't we make a small detour to Chapter 11 of the Bank of Spain's Statistical Bulletin, on General government liabilities. Excessive Deficit Procedure (EDP) debt. Now if we examine section 11.3 Liabilities outstanding and debt according to the excessive deficit procedure. Absolute values, we will find this most iluminating table.

Now, on the public accounts issue, I actually started digging into all this in the summer of 2010, and indeed posted an interim "report" at the time. So it is something of a mystery to me why all the hedge funds, journalists and bank analysts have taken so long in waking up to "Spain's regional debt problem", especially since all the information on the topic is freely available on the Bank of Spain website. It seems to me, that people see what they want to see at any given point in time, and this is the point of the Petrarch quote which starts this post. It comes from an Edgar Allen Poe short story, the purloined letter, and to cut a long issue short, a letter goes missing which no one can find, and the reason they cannot find it is precisely because it is lying their before them, on the living room mantelpiece.

If you try to go rummaging round for Goldman Sachs style interest rate swaps in

But before we did down any deeper, just to let us all see where we are, why don't we make a small detour to Chapter 11 of the Bank of Spain's Statistical Bulletin, on General government liabilities. Excessive Deficit Procedure (EDP) debt. Now if we examine section 11.3 Liabilities outstanding and debt according to the excessive deficit procedure. Absolute values, we will find this most iluminating table.

{kind=link}

Two important points should be drawn to the attention of the studious reader immediately, the fact that the right hand section refers to the Excess Deficit Procedure (EDP or officially recognised Eurostat) debt, and that the totals at the bottom of columns one and 15 are different. The number at the bottom of column one is approximately 877 billion Euros (or around 85% of Spanish GDP) while the number at the bottom of column 15 is 706 billion Euros, and this is the official Eurostat debt. So what makes for the difference? Well, as we will see, there are three main items - unpaid bills, public company debt, and Spanish sovereign bonds which are in the hands of the Social Security Reserve Fund. Now before going into all this further, I do want to make clear that I am not saying that this 877 billion euros is the total Spanish debt which should be counted as such. The number is simply orientative - a lot, but not all, of this is debt which will need to be consolidated - but in fact there are other "contingent liabilities" which will also need to be added in.

{kind=link}

But let's go one step at a time, and why not start with those famous "unpaid bills". Well, according to the Financial Accounts, at the end of the third quarter there were 72.9 billion Euros in unpaid bills (around 7% of GDP) which were more than 30 days overdue owed by the entire public adminstration (see this file here, bottom right second page - in fact there is a total of 87.5 billion Euros owing, but 14.6 billion is still within the term of normal trade credit). This breaks down as 27.7 billion Euros on the part of central government, 20.8 billion Euros from the regional governments, and 14.9 billion Euros for the local authorities. Much of this debt has been pending for months, if not years.

{kind=link}

The second main area of non-consolidated debt is the money owed by public companies, many of them loss making, and often entities which have been created without rhyme or reason. As of the end of the third quarter of 2011 this amounted to 57 billion Euros (or 5% of GDP - see the memorandum item on the far right in this file), of which 32 billion Euros was attributable to central government, 15.5 billion Euros belonged to regional governments, and 9.4 billion Euros came from companies created by local authorities.

{kind=link}

Then we come to the social security reserve fund. Ai, the social security reserve fund! This is where the Spanish are supposed to be accumulating resources to help pay for their pensions. But the Eurostat accounting system being what it is, this is the last thing that is happening. Now according to this last report from the fund managers, at the end of 2010 the fund had assets valued at just under 65 billion Euros under its charge. Of this sum 56.6 billion Euros (or over 5% of GDP) were invested in Spanish government bonds, while 7.8 billion Euros were invested in bonds of other EU states (principally Germany , the Netherlands and France

{kind=link}

Now doubtless the only reason the fund decided to invest the money it was holding in Spanish government bonds wasn't to help the administration hide debt, probably the fact that risky Spanish bonds pay more than less risky German ones was also a consideration. But this whole thing is a farce, since while the Spanish people innocently believe that they have a partially funded pension system, nothing could really be farther from the truth. In general accounting terms the whole security area comes under the general budget, as was brought to light in the recent deficit numbers the new government brought to light at the start of January. 0.5% of GDP in unexpected deficit came from issues in the social security fund - which anticipated a surplus of 0.4% of GDP but came in with a deficit of 0.1% of GDP, as can be seen in the nice chart provided by the Ministry (below).

{kind=link}

So we really have a clear "robbing Peter to pay Paul" type situation, where the numbers are juggled but the debt remains. This risks associated with this situation was brought to light in the recent Greek debt restructuring, since one of the key issues driving Greek politicians to the negotiating table was the threat of seeing their pension fund reserves going up in smoke in the event of a hard default.

According to the Wall Street Journal:

"The total portfolio of Greek bonds that the Greek pension funds hold is EUR27 billion," Venizelos said. "That portfolio is being replaced with cash, with new, better bonds of much higher net present value and, further, the parliament has already approved the creation of a special public body through which to transfer public assets to the funds," he added.And to Bloomberg:

According to the Wall Street Journal:

"The total portfolio of Greek bonds that the Greek pension funds hold is EUR27 billion," Venizelos said. "That portfolio is being replaced with cash, with new, better bonds of much higher net present value and, further, the parliament has already approved the creation of a special public body through which to transfer public assets to the funds," he added.And to Bloomberg:

"The country's central government debt, which doesn't include debt from local government organizations, state-run companies or pension funds, was 368 billion euros at the end of 2011, the ministry said today, amounting to 171 percent of the economy, according to Bloomberg calculations".

And Then There Are The Contingent Liabilities

The trouble is, this still isn't everything. We have the contingent liabilities to think about. This - a groso modo - comes in four forms: bank debt guarantees, exposure to the financial system via FROB, the government Instituto de Credito Oficial (ICO) and the Electricity Tariff Fund FADE.

On the bank guarantee side, the latest data we have is 88.6 billion Euros at the end of the third quarter of 2011, but this number is almost certainly higher now, since the government has been guaranteeing bonds with the unique objective that they could be taken over to the ECB as collateral in the LTROs. In any event, it is the Spanish state (and not the ECB) that is finally responsible for these loans should the relevant bank be unable to live up to its commitments.

On FROB the extent of real exposure is hard to measure, since while the quantity actually provided by the fund is not large at this point (and some of that was pre-capitalised) a number of savings banks are effectively nationalised while others that are dependent on FROB for loans may well need further intervention. So all we can safely say here is that the number involved is hardly trivial, and on just how "non trivial" the final number is the whole future ofSpain

As far as the ICO goes, the organisation currently has an exposure of 27 billion Euros, all guaranteed by the state. Now much of this money has gone out in lending, and much of that lending will be returned, which is why this is a contingent liability.

The trouble is, this still isn't everything. We have the contingent liabilities to think about. This - a groso modo - comes in four forms: bank debt guarantees, exposure to the financial system via FROB, the government Instituto de Credito Oficial (ICO) and the Electricity Tariff Fund FADE.

On the bank guarantee side, the latest data we have is 88.6 billion Euros at the end of the third quarter of 2011, but this number is almost certainly higher now, since the government has been guaranteeing bonds with the unique objective that they could be taken over to the ECB as collateral in the LTROs. In any event, it is the Spanish state (and not the ECB) that is finally responsible for these loans should the relevant bank be unable to live up to its commitments.

On FROB the extent of real exposure is hard to measure, since while the quantity actually provided by the fund is not large at this point (and some of that was pre-capitalised) a number of savings banks are effectively nationalised while others that are dependent on FROB for loans may well need further intervention. So all we can safely say here is that the number involved is hardly trivial, and on just how "non trivial" the final number is the whole future of

As far as the ICO goes, the organisation currently has an exposure of 27 billion Euros, all guaranteed by the state. Now much of this money has gone out in lending, and much of that lending will be returned, which is why this is a contingent liability.

{kind=link}

Finally, we have the so called Tariff Deficit fund, or FADE. One thing debt doesn't do here is fade (away), since it is growing every month and every year. This is described in the literature as a debt being accumulated by consumers (some 24 billion Euros of it) which is guaranteed by the government. Like the state of their savings in the pension system, most electricity consumers are totally ignorant of the fact that they are acquiring this debt, or better put, that it is being acquired on their behalf. Essentially the situation arises since the government is reluctant to charge an economic price for electricity. Naturally, in a country running an energy driven current account deficit this is a highly questionable practice, but then, there you are.

So basically every month less money comes in in bills than is attributed to the accounts of the electricity companies. The shortfall is made up by borrowing. This borrowing is serviced - you got it - by taking some of the income from electricity bills. But naturally, as the deficit grows - currently it is about 24 billion Euros - more of the income stream is needed to service the exisiting debt, and - yup, you got it again - the deficit grows. The only real solution to this mess is to raise electricity tariffs, but in an environment of rising unemployment and falling wages there are going to be limits to what the government can do. So while I am sure that the EU will eventually insist tariffs are raised, it is hard to see them being raised far enough to pay off the accumulated debt, and so the government will almost certainly need to "swallow" this, which means - yup you got it again - another 2% or so on the debt account.

MuchAdo

Now as Victor Mallet says, the basic motivation behind recent moves on the Spanish deficit front would seem to be to start to move this large backlog of debt onto the table.

Madrid

"It's about restoring order, it's about knowing what's there and dealing with it once and for all," Maria Soraya Sáenz de Santamaría, deputy prime minister, said after a cabinet meeting on Friday that agreed the first part of the programme.

So basically every month less money comes in in bills than is attributed to the accounts of the electricity companies. The shortfall is made up by borrowing. This borrowing is serviced - you got it - by taking some of the income from electricity bills. But naturally, as the deficit grows - currently it is about 24 billion Euros - more of the income stream is needed to service the exisiting debt, and - yup, you got it again - the deficit grows. The only real solution to this mess is to raise electricity tariffs, but in an environment of rising unemployment and falling wages there are going to be limits to what the government can do. So while I am sure that the EU will eventually insist tariffs are raised, it is hard to see them being raised far enough to pay off the accumulated debt, and so the government will almost certainly need to "swallow" this, which means - yup you got it again - another 2% or so on the debt account.

Much

Now as Victor Mallet says, the basic motivation behind recent moves on the Spanish deficit front would seem to be to start to move this large backlog of debt onto the table.

"It's about restoring order, it's about knowing what's there and dealing with it once and for all," Maria Soraya Sáenz de Santamaría, deputy prime minister, said after a cabinet meeting on Friday that agreed the first part of the programme.

But the great risk they are taking in doing this is raising the acknowledged debt level, up towards the "high risk area" around 100% of GDP.

Her mind in torment, wheeling like some lion at bay, dreading the gangs of investors and bond traders closing their cunning ring around her ready for the finish, Angela thrashed around looking for the rules and pacts that would save her embattled army. To no avail, her chariot struck a a rock which, like the one to the west of Grosseto which saw-off the unfortunate Costa Concordia along with her Captain, was on no known map, having not previously been measured, and she went hurtling down her crazed path towards a preappointed destiny with both history and oblivion.

PD1: Las gestoras extranjeras siguen creciendo en volumen. Son mejores que las domésticas, por mayor volumen de sus fondos y por la especialización y expertise de sus gestores:

CNMV: las gestoras extranjeras tienen un patrimonio de 37.600 millones de euros :Según los últimos datos de CNMV, correspondientes al cierre del primer trimestre de 2011, el volumen bajo gestión de las gestoras extranjeras en España habría aumentado un 22% desde marzo de 2010 a marzo de 2011, situándose en 37.639 millones de euros (desde los 30.864 millones de doce meses antes).

Principales magnitudes IIC extranjeras

| |

Número de IIC

|

669

|

Partícipes

|

855.929

|

Volumen de inversión

|

37.639

|

Fuente: CNMV. Datos a marzo de 2011. El volumen, en millones de euros | |

PD2: Francisco González vende sus acciones de BBVA. Vamos a ver, si eres presidente de un banco y cobras en acciones, no vendas que das un ejemplo malísimo. Si ni siquiera el presidente se queda con sus acciones, ¿quién se las quedará? No me creo que necesites dinero, caja, para nada. Si Botín vendiera sus acciones, ¿qué diríamos? Estos banqueros tan bien remunerados, ¿son de los que trincan la pasta y salen corriendo? Ahhh, vale macho…

PD3: Me gustaría ofrecerte esta imagen de la Virgen María , esperanza de Oriente:

Del autor: JAVIER VIVER:

http://www.larazon.es/noticia/8367-mis-obras-de-arte-transforman-a-la-gente

http://larazon.es/noticia/8402-el-reto-era-lograr-una-imagen-imbuida-en-la-eternidad

¿No sería mejor tener una bonita imagen de la Virgen que no las cantidades de tontadas que tenemos en los hogares? Para ponerle flores y rezarle…