La clase media está sufriendo y mucho más que va a sufrir si volviéramos a las andadas en esta larga crisis de deuda que vivimos… Nos costó muchos años de generosidad crear un sistema de bienestar público, un reparto de los dineros hacia todos, haciendo una sanidad y educación universal, y provocando una amplia clase media con capacidad de compra importante.

Pero hubo tantos excesos que nos explotó la burbuja del crédito en la cara. Se optó por salvar a la banca, de hacer una devaluación interna (bajada de precios en inmuebles y de los salarios y beneficios empresariales), lo que ha provocado un socavón en la clase media. Además, se pretende que la salida de la crisis parte de la misma vieja premisa: que aumente el consumo, gracias a la facilidad, de nuevo, del crédito… Volvemos a las andadas…

Ya hemos visto como la clase media a desaparecido en otros países como Grecia, que van muy por delante nuestro. Pero una ruptura del euro, una nueva fuerte subida de la prima de riesgo, un rescate al Reino de España, rescate que se haría a costa del sistema bancario español, ya que los contribuyentes alemanes ya no van a pagar ni un céntimo más en ayudar a otros, generaría un país con una muy menguada clase media. Unos pocos, los que se preparen para preservar el capital, serían los ricos del futuro. Otros muchos dejarían de ser considerados clase media y volverían a meramente subsistir…

A ti, ¿cómo te pilla, andas preparado para lo que pueda venir, serás de los que se están preparando para evitar el “gran susto” que nos puede llegar? Si vives tranquilo, es que eres un iluso, o no te has preparado para evitar ese evento que nos empobrezca y nos deje mucho peor de cómo estuvimos en 2008 o 2012… Los gobernantes han ganado tiempo, escarceos intermedios, pero no la batalla final…, a la que esperamos.

En otro países ocurre justo al revés. Empieza a florecer una clase media con capacidad de compra, que se va a gastar su alta renta disponible en las mismas memeces que nos hemos gastado los occidentales nuestro dinero en los últimos 30 años…

Según el Círculo de Empresarios:

EL GRÁFICO… EXPANSIÓN DE LA CLASE MEDIA GLOBAL, 2030

En 2009, un cuarto de la población mundial, 1.845 millones de personas, se clasificaba como clase media al disponer de unos ingresos diarios de entre 10 y 100 dólares (1) . Un 60% de este segmento poblacional residía en economías desarrolladas.

En las próximas dos décadas la clase media global representará entre el 50% y el 66% de la población mundial (2), debido principalmente a su crecimiento en los países emergentes.

Por regiones, de las 1.845 millones de personas, 525 millones se localizaban en Asia-Pacífico, con 150 millones en China y 50 en India.

Analizando su evolución hasta 2030, el mayor incremento de la clase media se producirá precisamente en Asia-Pacífico, donde se concentrarán dos tercios de la clase media global (3.228 millones) y un 59% de su consumo total. Liderarán este boom China e India, con 1.000 y 475 millones de personas, respectivamente.

En contraste, en Norteamérica y Europa previsiblemente se producirá un ligero retroceso de la clase media y de su peso sobre el total global, entre otros factores por el envejecimiento de su población.

Desde el punto de vista económico y social, su expansión tiene efectos positivos y directos sobre el crecimiento, desarrollo y bienestar de un país. Así, según el economista Surjit Bhalla, por cada 10 puntos porcentuales de incremento de este segmento poblacional, se produce un aumento de medio punto en la tasa de crecimiento económico.

(1) Ernst and Young: “Hitting the sweet spot: The growth of the middle class in emerging markets”.

(2) The Expanding Middle: The Exploding World Middle Class and Falling Global Inequality, Goldman Sachs, 2008; y Homi Kharas y Geoffrey Gertz, The New Global Middle Class: A Cross-Over from West to East, Wolfensohn Center for Development, 2010.

Dentro del mundo emergente, estas son las previsiones de crecimiento de la clase media:

Abrazos,

PD1: Y en esta desaparición de la clase media occidental tiene mucho que ver el EFECTO MILLENNIALS

The Federal Reserve conducted a study on Millennials and tried to ascertain why so many of them are living at home. Is it too much student debt? Lower incomes? Or is it that home prices aresimply unaffordable? The study finds that all of these factors have a big impact on why many Millennials are living at home and why the first time home buyer market is performing so badly. It also gives us insight into the shifting building demand of new construction. Many builders are focusing their energies on multi-unit structures to cater to an audience that will look for rentals or lower priced condos. There is a heavy renting trend undertaking this country. We are seeing a record numbers of young people living at home with mom and dad heading directly back into their childhood rooms to rock out the NES and attempting to pass Super Mario Brothers once again. There are major implications for housing because of this new structural change. First time home buying is down dramatically. Construction is catering to a lower income cohort. Let us look at what the Fed found in their report.

The massive number of young adults living at home

One of the interesting findings is that the trend of young adults living at home has continued on an upward slope going all the way back to 1999. Even the toxic mortgage days of Housing Bubble 1.0 didn’t really shift this figure by much. But the homeownership rate increased which means that the push came from older cohorts or young buyers that had the misfortune of buying near the top (and of course many wereburned in epic fashion).

So let us look at the findings:

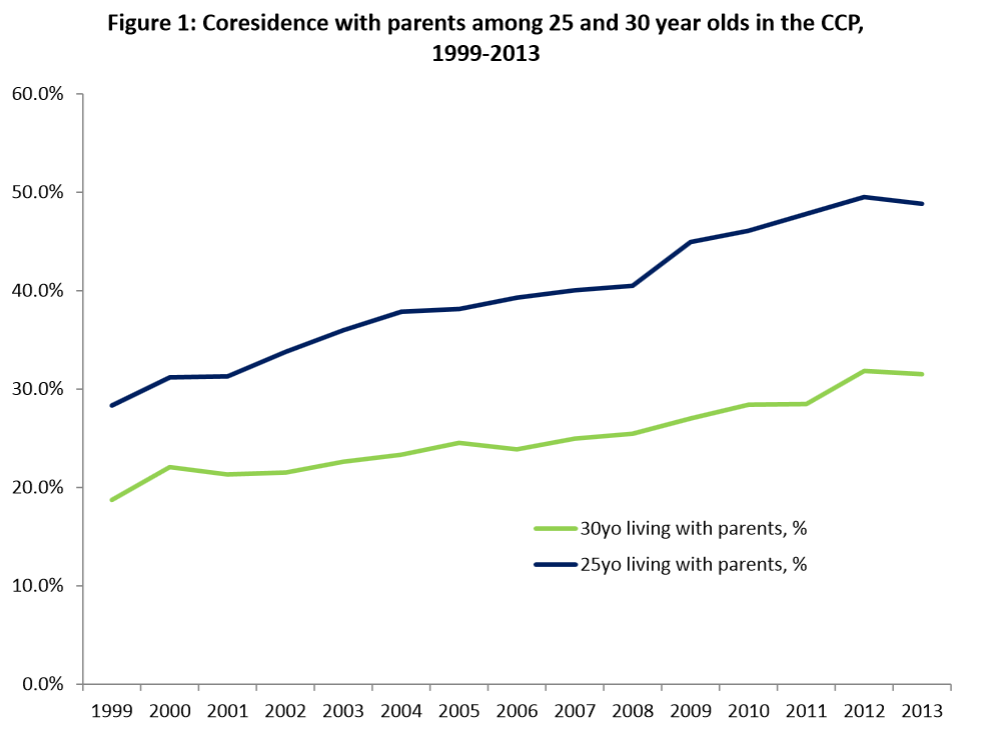

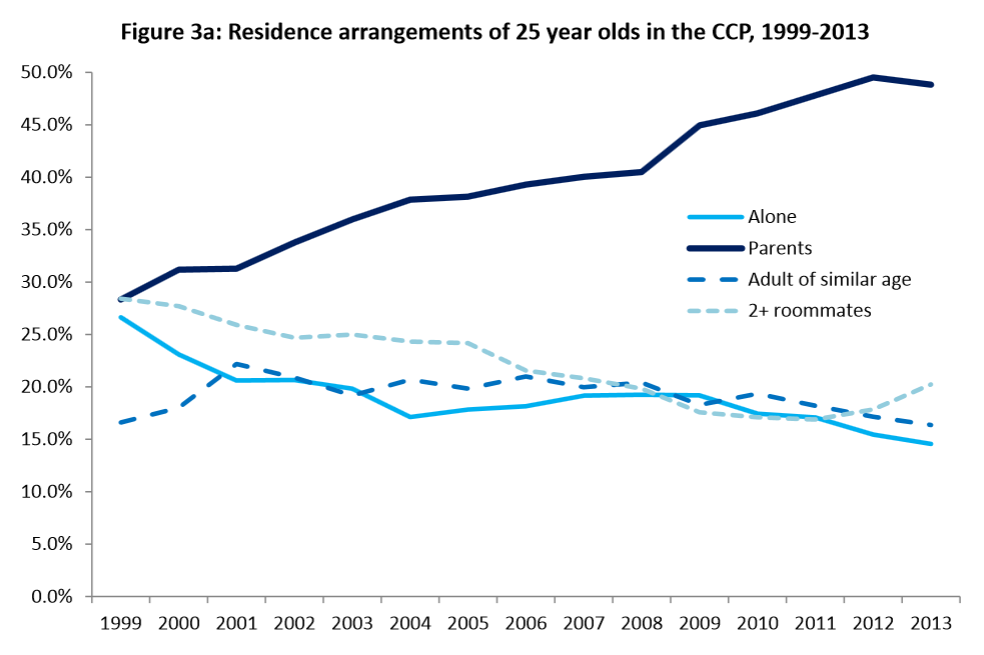

Nearly half of those 25 years of age are living at home with parents. The rate is up to 30 percent for those 30 years of age. These are dramatic increases from 1999. There has been paltry data on the makeup of housing composition because some were saying that many were shacking up with roommates. That does not appear to be the case:

If you were placing a bet, you would be in a good position putting your money on those 25 years of age living at home with parents. The first time home buyer market continues to perform pathetically. Of course, with investors pulling back we now have the FHFA trying to push for 3 percent down payment loans to get the juices flowing again. We are already at 5 percent down payments so this move to 3 percent will likely offer minimal help for younger Americans.

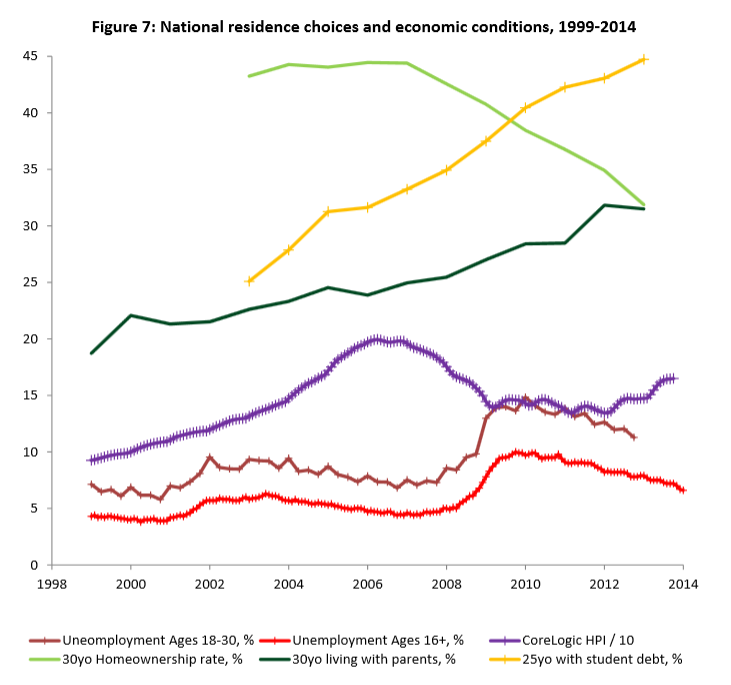

One of the better graphs from the Fed report is the combination of all these factors into one spot:

The homeownership rate of the 30 year old cohort has tanked starting in 2007 with the market implosion. That is very clearly illustrated by the green line above. Why? These were the folks buying with toxic mortgages and timed the market very poorly (or simply had bad luck). The rate of those young adults living at home has gone up unabated since 1999. Of course the increase in home prices has been driven by investors and this will simply make it harder on a cohort with lower incomes and much higher levels of student debt.

It is safe to say that many more young Americans will be renting deep into their adulthood. It is also safe to say given the current cost of college that many more young Americans will be coming back home to live with mom and dad. The Fed’s findings are simply reinforcing this trend.

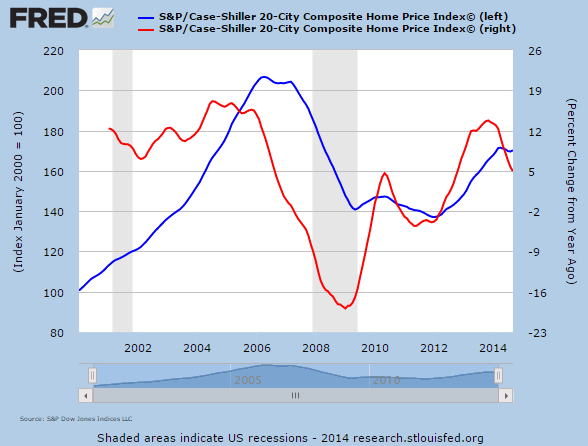

Given the boom and bust nature of housing, we already see that the rate of price increases is slowing down very quickly:

The pattern seems to be clear. Prices ramp up. The economy hits a hiccup. And prices come trending lower. This even happened in the 2010 to 2012 period. Look at where we are at right now. And the recent run up in 2013 was largely driven by a fickle group in investors.

Millennials are living at home for the following reasons:

-Heavy levels of student debt

-Lower wages

-Inability to afford current home prices and in many markets, current rents

So how this sets up for a pent up demand for expensive homes or nicely painted crap shacks is really beyond the data. The demand will be from older Friskie eating households, investors, and foreign buyers. It was interesting to see the number of EB-5 visas being pumped out largely to those from China:

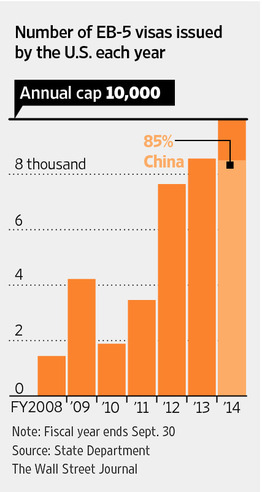

“(WSJ) To finance the concrete-steel platform, Related tapped a little-known and at times controversial federal visa program known as EB-5, which offers green cards to foreign families who invest at least $500,000 in U.S. projects that create at least 10 jobs per investor.”

It doesn’t even have to be 10 jobs necessarily but the hours have to work-out to the equivalent of 10 jobs. I’ve heard of people buying places like yogurt stores or fast food chains. Not exactly 10 great paying jobs but enough to keep young adults living at home with mom and dad. Since real estate volume is low margin in some markets, even having a few hundred buyers in one area can shift prices dramatically:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

“(WSJ) These investors aren’t coming for the investment,” said Yi Song, a New York lawyer who works with Chinese clients. “They are coming here for their children to obtain a better education and to get residence as an insurance policy.”

The EB-5 program was virtually non-existent in terms of volume even just a few years ago. That is no longer the case. But again, the demand isn’t coming from younger Americans that are suddenly making so much money that they are buying real estate. Short of better paying jobs, the first time buyer market is going to have a tough time.

PD2: La clase media de EEUU tiene problemas también. Mira el New York Times lo que dice:

The American Middle Class Is No Longer the World’s Richest

The American middle class, long the most affluent in the world, has lost that distinction.

While the wealthiest Americans are outpacing many of their global peers, a New York Times analysis shows that across the lower- and middle-income tiers, citizens of other advanced countries have received considerably larger raises over the last three decades.

After-tax middle-class incomes in Canada — substantially behind in 2000 — now appear to be higher than in the United States. The poor in much of Europe earn more than poor Americans.

The numbers, based on surveys conducted over the past 35 years, offer some of the most detailed publicly available comparisons for different income groups in different countries over time. They suggest that most American families are paying a steep price for high and rising income inequality.

Although economic growth in the United States continues to be as strong as in many other countries, or stronger, a small percentage of American households is fully benefiting from it. Median income in Canada pulled into a tie with median United States income in 2010 and has most likely surpassed it since then. Median incomes in Western European countries still trail those in the United States, but the gap in several — including Britain, the Netherlands and Sweden — is much smaller than it was a decade ago.

In European countries hit hardest by recent financial crises, such as Greece and Portugal, incomes have of course fallen sharply in recent years.

The income data were compiled by LIS, a group that maintains the Luxembourg Income Study Database. The numbers were analyzed by researchers at LIS and by The Upshot, a New York Times website covering policy and politics, and reviewed by outside academic economists.

The struggles of the poor in the United States are even starker than those of the middle class. A family at the 20th percentile of the income distribution in this country makes significantly less money than a similar family in Canada, Sweden, Norway, Finland or the Netherlands. Thirty-five years ago, the reverse was true.

LIS counts after-tax cash income from salaries, interest and stock dividends, among other sources, as well as direct government benefits such as tax credits.

The findings are striking because the most commonly cited economic statistics — such as per capita gross domestic product — continue to show that the United States has maintained its lead as the world’s richest large country. But those numbers are averages, which do not capture the distribution of income. With a big share of recent income gains in this country flowing to a relatively small slice of high-earning households, most Americans are not keeping pace with their counterparts around the world.

“The idea that the median American has so much more income than the middle class in all other parts of the world is not true these days,” saidLawrence Katz, a Harvard economist who is not associated with LIS. “In 1960, we were massively richer than anyone else. In 1980, we were richer. In the 1990s, we were still richer.”

That is no longer the case, Professor Katz added.

Median per capita income was $18,700 in the United States in 2010 (which translates to about $75,000 for a family of four after taxes), up 20 percent since 1980 but virtually unchanged since 2000, after adjusting for inflation. The same measure, by comparison, rose about 20 percent in Britain between 2000 and 2010 and 14 percent in the Netherlands. Median income also rose 20 percent in Canada between 2000 and 2010, to the equivalent of $18,700.

The most recent year in the LIS analysis is 2010. But other income surveys, conducted by government agencies, suggest that since 2010 pay in Canada has risen faster than pay in the United States and is now most likely higher. Pay in several European countries has also risen faster since 2010 than it has in the United States.

Three broad factors appear to be driving much of the weak income performance in the United States. First, educational attainment in the United States has risen far more slowly than in much of the industrialized world over the last three decades, making it harder for the American economy to maintain its share of highly skilled, well-paying jobs.

Americans between the ages of 55 and 65 have literacy, numeracy and technology skills that are above average relative to 55- to 65-year-olds in rest of the industrialized world, according to a recent study by the Organization for Economic Cooperation and Development, an international group. Younger Americans, though, are not keeping pace: Those between 16 and 24 rank near the bottom among rich countries, well behind their counterparts in Canada, Australia, Japan and Scandinavia and close to those in Italy and Spain.

A second factor is that companies in the United States economy distribute a smaller share of their bounty to the middle class and poor than similar companies elsewhere. Top executives make substantially more money in the United States than in other wealthy countries. The minimum wage is lower. Labor unions are weaker.

And because the total bounty produced by the American economy has not been growing substantially faster here in recent decades than in Canada or Western Europe, most American workers are left receiving meager raises.

Finally, governments in Canada and Western Europe take more aggressive steps to raise the take-home pay of low- and middle-income households by redistributing income.

Janet Gornick, the director of LIS, noted that inequality in so-called market incomes — which does not count taxes or government benefits — “is high but not off the charts in the United States.” Yet the American rich pay lower taxes than the rich in many other places, and the United States does not redistribute as much income to the poor as other countries do. As a result, inequality in disposable income is sharply higher in the United States than elsewhere.

Whatever the causes, the stagnation of income has left many Americansdissatisfied with the state of the country. Only about 30 percent of people believe the country is headed in the right direction, polls show.

“Things are pretty flat,” said Kathy Washburn, 59, of Mount Vernon, Iowa, who earns $33,000 at an Ace Hardware store, where she has worked for 23 years. “You have mostly lower level and high and not a lot in between. People need to start in between to work their way up.”

Middle-class families in other countries are obviously not without worries — some common around the world and some specific to their countries. In many parts of Europe, as in the United States, parents of young children wonder how they will pay for college, and many believe their parents enjoyed more rapidly rising living standards than they do. In Canada, people complain about the costs of modern life, from college to monthly phone and Internet bills. Unemployment is a concern almost everywhere.

But both opinion surveys and interviews suggest that the public mood in Canada and Northern Europe is less sour than in the United States today.

“The crisis had no effect on our lives,” Jonas Frojelin, 37, a Swedish firefighter, said, referring to the global financial crisis that began in 2007. He lives with his wife, Malin, a nurse, in a seaside town a half-hour drive from Gothenburg, Sweden’s second-largest city.

They each have five weeks of vacation and comprehensive health benefits. They benefited from almost three years of paid leave, between them, after their children, now 3 and 6 years old, were born. Today, the children attend a subsidized child-care center that costs about 3 percent of the Frojelins’ income.

Even with a large welfare state in Sweden, per capita G.D.P. there has grown more quickly than in the United States over almost any extended recent period — a decade, 20 years, 30 years. Sharp increases in the number of college graduates in Sweden, allowing for the growth of high-skill jobs, has played an important role.

Elsewhere in Europe, economic growth has been slower in the last few years than in the United States, as the Continent has struggled to escape the financial crisis. But incomes for most families in Sweden and several other Northern European countries have still outpaced those in the United States, where much of the fruits of recent economic growth have flowed into corporate profits or top incomes.

This pattern suggests that future data gathered by LIS are likely to show similar trends to those through 2010.

There does not appear to be any other publicly available data that allows for the comparisons that the LIS data makes possible. But two other sources lead to broadly similar conclusions.

A Gallup survey conducted between 2006 and 2012 showed the United States and Canada with nearly identical per capita median income (and Scandinavia with higher income). And tax records collected by Thomas Piketty and other economists suggest that the United States no longer has the highest average income among the bottom 90 percent of earners.

One large European country where income has stagnated over the past 15 years is Germany, according to the LIS data. Policy makers in Germany have taken a series of steps to hold down the cost of exports, including restraining wage growth.

Even in Germany, though, the poor have fared better than in the United States, where per capita income has declined between 2000 and 2010 at the 40th percentile, as well as at the 30th, 20th, 10th and 5th

PD3: El BCE ha actuado al fin, ya hay estímulos monetarios. Pero espera a que el mercado le de un segundo pensado, que quizás no es tan interesante. Inyectan 60.000 millones de euros cada mes hasta sep/16. Pero con un matiz, el riesgo lo asume casi en la totalidad los bancos centrales nacionales (el BCE sólo asume el 8% de estas compras). ¿Qué quiere decir? Que el Banco de España es el que va a comprar ese 12,6% de cuota europea que nos corresponde a nosotros, de la nada. Se lo compra a los bancos que tendrán más liquidez. Como sabes la banca española tiene un problema de solvencia, no de liquidez, ya que le sobra, y la devuelve (los LTROs) al BCE. En definitiva, ¿creceremos más, darán más crédito los bancos españoles? Nole. Y encima, si las cosas se tuercen pagaremos los españoles, los europeos no han puesto un duro, sino que lo va a poner España directamente…, de la nada… Ridiculous!! Más ridículo es todavía para los países del núcleo duro, con intereses negativos, van a comprar esos bonos que dan intereses negativos a los bancos que no sabrán qué hacer con el dinero que les dan. ¿Seguirán comprando los bancos europeos deuda española/italiana, que les sale más rentable que la suya, y así hacen más beneficios con el carry trade? Explosivo…

Los ganadores: El Gobierno de España se frota las manos al saber que va a tener alguien comprando sus papelitos del Tesoro Público tan exitosamente como antes…, sin preguntas. Y con el plan de reformas y ajustes presupuestarios, que el BCE demanda, no se verán tan presionados ahora…, bueno estaban pasando y tal. Ahora ya tiene la pasta, luego las reformas pueden esperar para más tarde…

Los bancos comerciales: Les sobra la liquidez, ya que no hay demanda solvente de crédito. No obstante, saben que es cojonudo tener a alguien para chutarle sus posiciones de bonos españoles, por si se tuerce el mercado y tal… Han ganado una pasta en la deuda pública y ahora encima se la pueden ir vendiendo al Banco de España y cual…

Los perdedores: Los parados, que no reciben nada, los españoles en su conjunto, ya que esta inyección de liquidez no sirve para crecer, ni para reducir el total de deudas que acumulamos… Esta ingeniería financiera es mala y puede explotarnos en la cara en el futuro. ¿Se dará la vuelta alguna vez? ¿Tendrá que devolver el BCE, a través de sus bancos centrales locales, la pasta algún día, o la van a comprar para siempre? ¿Mario Dragui aguantará la presión alemana, que debe andar muy cabreada, o le obligarán a dimitir? Estamos llegando tarde y mal… Podemos ver nuevas turbulencias en el futuro derivadas de estos excesos. No somos EEUU. Y otros intentos de hacer QE, en este reciente pasado, no han funcionado (léase Japón, Suiza…)

Ya te lo dije esta mañana, no es la solución de los problemas de crecimiento en Europa. La subida del mercado, que seguirá, será hasta que se caigan del guindo. El dólar fuerte, no me extraña nada… Y de la deflación te hablaré el lunes…

PD4: Como sabes, la crisis no es sólo económica, es de valores, puro “postureo”: Culto al cuerpo y al dinero

El capitalismo se centra en tener, y este se convierte en un dios, y el único pecado de esa «religión» es perder dinero. Se refleja en la vida de la sociedad de una manera continuada. No nos preocupa lo que somos, es más, no sabemos en muchos casos lo que eso significa. Tener es lo importante. Nos quejamos de que los demás valoren a las personas por lo que tienen, pero en el fondo estamos todo el día dando signos externos para que nos valoren por lo que tenemos. Se cambia de coche cada cierto tiempo, o por lo menos lo pintamos de otro color, alguien picará y se creerá que es nuevo. Presumimos de cargo, de sueldo, de dinero, de vacaciones, de colegio de los niños, de lo que haya que presumir. Todo lo que sea necesario para demostrar que soy muy importante porque tengo muchas cosas, mucho poder; lo digo sin recato. Así, estando en ese positivismo exacerbado, pasamos sin darnos cuenta al utilitarismo en el cual se trata a las cosas como personas y a las personas como cosas. Es decir, se valora a las personas no sólo por lo que tienen materialmente, sino por lo que tienen físicamente. Esta valoración de lo físico hace que, en nuestra sociedad, las personas gasten mucho dinero y se sometan a mil sacrificios por cuidarlo.

La perfecta conjunción es mucho dinero y buen físico. Muchos darían su vida por ello, o al menos, parte de su vida. Encuestas hay que lo dicen. Además damos por seguro que las personas en esa situación son felices. ¿Nosotros porqué no lo somos? Nos faltan ceros en nuestra cuenta corriente y un poco más de belleza. Pero llegaremos. Hay que esforzarse, seguro, terminaremos teniendo muchas cosas y siendo guapos, o sea, felices. Realmente, cuando pido que me valoren por lo que tengo, lo que hago cada vez más, es convertirme en objeto, sobre todo en el terreno de la guapura, de lo físico. Cada vez que tengo oportunidad, expongo el físico y los demás desean lo que ven. Digo que el pudor no existe, que no me da vergüenza, lo expongo todo si puedo, en realidad me estoy exponiendo yo, luego en el fondo estoy pidiendo que se me trate como objeto. Cuando una persona pone todo su esfuerzo en mejorar lo que tiene, física y materialmente, lo que está diciendo es que se le valore por lo que tiene, o sea, como objeto. Cuando se acerca el verano los esfuerzos se redoblan. Así seré más deseado…

Cuando las cosas se exponen, se dice que están en escaparate. Para eso están los escaparates, para que la gente vea cosas y las desee. Y cuando se canse las deje. Eso estoy haciendo yo. Además, de lo que hay en los escaparates, la gente habla, opina, compara. No me puedo quejar. Yo quiero ser tratado así. Mi intimidad es lo que se ve. Sería mucho pedir que en unas cosas te traten según lo que eres y en otras según lo que tienes. Porque con tu vida estás diciendo, que lo que eres es lo que tienes y lo que tienes es lo que se ve, lo que expones al público para ser visto. ¡Ah!, supongo que no queremos ser queridos de esa manera. Es una contradicción. A la gente se la quiere por lo que es. Cuando el foco está sólo en tener, la gente va a ver qué saca, que pilla. ¡Luego dices que eres feminista o que estás a favor de la mujer! Así es imposible querer y ser querido. El fracaso de toda una civilización en su lucha por encontrar la felicidad, se está viendo en las tasas de divorcios.