Se les ha dado estos nombres a las tres generaciones de personas que trabajan en EEUU. ¿En cuál te encuadras tú? Alguno de estos grupos las están pasando putas, o las van a pasar peor incluso… El “New Normal”, es decir, cómo quedaremos después de la crisis de deuda, no se va a parecer en nada a como estábamos antes…

We have extensively covered the economic devastation that currently plagues the largest...

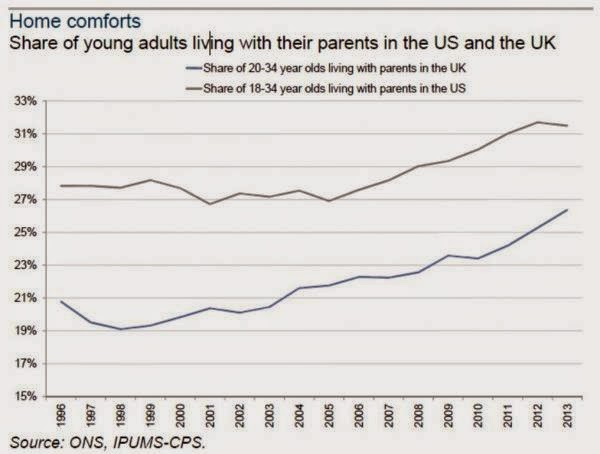

... and most important age for the future of the nation cohorts in the US: adults under 35, also known as Millennials. For a refresher see Millennials Devastated As American Dream Becomes Nightmare For Most, On Crushing Student Loans, Worthless College Degrees And The Millennials, Dear Recently Graduated Millennials: Prepare To Work Until You Are 73, and of course, Meet The Millennials: All You Ever Wanted To Know About America's Youth, In Charts.

Today, we present the latest nail in the coffin of the generation which none other than Obama said he is betting on to "Help Shape the New American Economy."

The bottom line, or rather, negative line, is the Millennials' savings, because "after a flirtation with thrift after the recession, young Americans have stopped saving. Adults under age 35—the so-called millennial generation—currently have a savings rate of negative 2%, meaning they are burning through their assets or going into debt, according to Moody’s Analytics. That compares with a positive savings rate of about 3% for those age 35 to 44, 6% for those 45 to 54, and 13% for those 55 and older."

The turnabout in savings tendencies shows how the personal finances of millennials have become increasingly precarious despite five years of economic growth and sustained job creation. A lack of savings increases the vulnerability of young workers in the postrecession economy, leaving many without a financial cushion for unexpected expenses, raising the difficulty of job transitions and leaving them further away from goals like eventual homeownership—let alone retirement.

“In the very near term it’s a plus for spending and economic growth, but in the long run these households are not saving, and that will impair their ability to spend in the future,” said Mark Zandi, the chief economist of Moody’s Analytics who calculated the numbers with Moody’s economist Mustafa Akcay.

... the new Moody’s data—using a technique developed at the Federal Reserve to combine its Survey of Consumer Finances and Financial Accounts of the United States reports—show how savings rates diverge across demographic groups.

Here is the problem: recall that Janet Yellen's "suggestion" to defeat record wealth inequality is for "poorer" Americans to build assets. Well, there is a problem when you can't even save enough to have $1 left in your pocket at the end of the month after all expenses:

“I’ve been saving almost exclusively in my mind,” said 26-year-old Emily Turner, a 2010 graduate of Villanova University who lives in southern Maryland. Most of her paycheck from the digital consulting and web-design firm she works for “doesn’t even make it to a conventional bank account. I’ve certainly not had the opportunity to invest in stocks or anything.”

The rest is well-known to regular ZH readers:

The problems from a lack of savings promise to reverberate for years. Those who don’t save are unlikely to be wealthy in the future, meaning American angst over wealth inequality seems poised to persist if most millennials are unable to save or choose not to.

Young households’ wealth has declined even more than their incomes. In the previous generation, Americans who were under 35 in 1995—often labeled Generation X—earned wages that were 9% higher than today after adjusting for inflation. Now, the median millennial has a net worth of $10,400, down 42% from $18,200 for Generation X, according to Fed data.

Why the disastrous economic data for America's most important generation? The answer is simple: the economy is, despite all the pomp and propaganda, still a disaster. That, and of course, the $1.2 trillion student loan bubble.

For some young households, the inability to save reflects the weak job market, said Shai Akabas, an economist at the Bipartisan Policy Center. While unemployment nationally has fallen below 6%, workers age 25 to 34 have a 6.2% unemployment rate and those 20 to 24 face 10.5% unemployment.

“There’s people who really can’t save because they don’t have the means to save and that’s not a small group of people,” Mr. Akabas said. “If you’re in a $25,000-a-year job and starting a family, it’s going to be very hard to accumulate savings regardless of your consumption decisions.”

Another big difference from earlier generations is the rise of student loans. In 1995, borrowers under 35 had median student debt of $6,100, according to Fed data. That has risen to $17,200.

For Ms. Turner, debts include $5,000 in student loans, $3,000 on credit cards and $6,000 borrowed from family. “There’s no formal note for that, but it resides in my psyche that I will pay it back at some point,” she said.

“I know I shouldn’t have accepted credit so freely,” she said. “But part of youth, the wiring of a young person, is the focus on really short-term gratification.”

And then there is also the fact that Millennials just prefer to live well:

The money mostly went to her social life and travel, [Emily Turner] says: a trip to Central America, a wedding in Southern California, a bachelorette party in Austin, Texas, trips to Atlanta and Charlotte, N.C., to see friends, another bachelorette party in Austin.

There was a sign it wouldn’t be this way. After the recession, the savings rates of those under age 35 climbed to 5.2% in 2009 and even briefly surpassed the savings of those age 35 to 44, according to Moody’s.

Don't worry Emily, soon enough you won't have the ability to fund such distractions at which point you can once again focus wholeheartedly on boosting your savings. Best of luck.

Why I’m Betting on You to Help Shape the New American Economy

History has dubbed you the “Millennials.”

You’re part of the first generation to grow up in the digital age. Some of you grew up with cell phones tucked into your book bags, while others can remember the early days of landline, dial-up internet. You’ve gone from renting movies on VHS tapes to purchasing and downloading them in a matter of minutes.

Today, more of you are earning college degrees than ever before — and more young people from low-income families are getting a shot at higher education than previous generations. Along with having higher education levels, you’ve got a lower gender pay gap than other generations?—?and we’re working to close it even further. Take all those things together, and it’s no surprise that entrepreneurship is in your DNA. One survey found that more than half of Millennials expressed interest in starting (or have already started) their own business.

So here’s something we know for certain: Your rising generation of Americans isn’t just adapting to a 21st-century economy. You’re actively changing it.

And we know that when we invest in your potential, rather than stack the deck in favor of the folks who are already at the top, our entire economy does better. It’s the reason we’ve expanded grants, tax credits, and loans to help more families afford college. It’s why we’re giving nearly 5 million Americans the chance to cap student loan payments at 10 percent of their income. And thanks to the Affordable Care Act, the number of uninsured young adults has fallen by nearly 40 percent over the past four years.

You may have graduated into the worst recession since the Great Depression, but today — for all the challenges you’ve already faced, and after all the grueling work it’s taken to bounce back — you’re in the best position to break into the newest sectors of the new American economy.

...

Throughout my time in office, my Administration has bet on American innovation. We’ve bet on America’s young people. And today, I’m betting that you’ll continue unleashing new ideas and new enterprises for decades to come.

And that's why, dear young Americans, you are fucked.

Abrazos,

PD1: Y mientras nosotros preocupados por las consecuencias de la inmigración…

Heated political debate obscures economic impact of immigration

Given the rambunctious immigration debate in countries around the world, it is tempting to believe that the globe is awash with migrants.

Whether it is the heated debate in the US over President Barack Obama’s move to normalise the status of some 5m illegal migrants or the wriggling of political elites in response to the rise of anti-immigrant parties in Europe, it is hard to find a country in the rich world where immigration does not sit near the top of the political agenda.

There are certainly signs that, as the global economy recovers unevenly from the effects of the 2008 global financial crisis and the economic malaise that followed, some migrants are seeking opportunities in those countries where the recovery is strongest. Britain last week reported that net migration reached a record 260,000 in the year to June 2014, a result derided by critics as a government failure and hailed by business groups as a needed tonic for a recovering economy.

But, viewed globally, the situation is neither as simple nor as new as the heat in the political debates might have you think. In fact, when you consider the data, migration today looks more like an odd paradox of globalisation than a consequence of it.

We live in a globalised world in which the opportunities for mobility are much greater than before. However, the reality is that we are just as prone to stay home as we were half a century or more ago. There are more migrants today than there have ever been – more than 232m, according to the UN. But then there are more people in the world than at any other time.

Today, as was the case in 1960 and as has largely been true for the five decades since, just 3 per cent of the global population live outside the country of their birth.

“Why is it that 97 per cent of the world population doesn’t migrate, at least internationally?” asks Mathias Czaika, a researcher at Oxford university’s International Migration Institute.

“The phenomenon is not migration. The phenomenon is non-migration.”

That, he argues, should be at the core of the political debate. But politics have always been volatile in economic downturns and history tells us that migrants have often been targets for the disgruntled when economies slow.

The reality is that migration in history tends to track economic opportunity and that this time is no different.

According to UN data, there are now a million less migrants in the world each year – 3.6m on average in recent years – than there were before the crisis. According to the OECD, the number of migrants seeking jobs in its predominantly rich member countries almost halved from 4.4 persons per thousand population in 2005-08 to 2.6 persons per thousand in 2009-2012.

Illegal migration, often driven by a search for economic opportunity, also appears to have slowed in recent years in the US and Europe. In the EU, illegal immigration has fallen largely as a result of the expansion of the union and the drawing in of countries such as Romania that had at one time been big sources of illegal migrants.

People continue to flee conflict: more than 3m people have registered as refugees from the war in Syria alone. But the great migrations today are taking place inside countries rather than across borders.

China has 200m more urban residents than it did a decade ago and plans to house 100m more migrants from rural areas in its cities by 2020. The world as a whole now has a little over 230m international migrants and added 77m between 1990 and 2013, according to UN data. There is a vast difference in rate also. China is urbanising at a rate of 1.8m new city residents each month, according to the World Bank. The US, which remains the biggest destination for immigrants, gains just over 1m new legal immigrants each year.

Spend some time looking at the data and it becomes clear that politicians may be having the wrong immigration debate.

Global movement: Steady flows

There are more people living outside their home country than ever, with the UN classifying 232m people as international migrants in 2013. But that is largely a result of population growth. Since 1960, the percentage of the global population classified as migrants has remained steady at roughly 3 per cent.

Arrivals and departures: American dream reigns while Indians and Bangladeshis lead exodus

The US remains by far the biggest destination for migrants. There are now almost 46m people in the US classified as international migrants, or one in six of the population. India and Bangladesh have been the biggest net exporters of people in recent years.

Crisis takes toll: Slowdown restricts movement

The crisis of 2008 had a big impact on migration, with a million fewer people a year moving to another country on average after 2010 than in the 10 years before, when the average was 4.6m, according to the UN. Average net migration between OECD countries fell to 2.6 persons per thousand in 2009-12, according to the OECD.

Traffic signals: US tightens border with Mexico

The US-Mexico border is the world’s biggest immigration corridor. But both legal and illegal immigration have slowed. In the 1990s, more than 500,000 migrants a year crossed into the US from Mexico. Since 2010, that number has fallen below 200,000 a year, according to UN data.

Levelling off: Downturn deters illegal workers

Illegal migration to the US has fallen in recent years – a phenomenon that some economists attribute to dwindling economic possibilities since the 2008 crisis. According to the Pew Research Center, the US’s population of illegal immigrants has stabilised just above 11m in recent years after peaking at 12.2m before the crisis.

Continental shift: EU anxieties drive churn

The crisis in the EU has caused significant churn in its migrant population. Those countries hit the hardest by the economic crisis, such as Greece and Spain, have seen significant net emigration in recent years. Countries that have done better economically, such as Germany and the UK, have attracted more migrants.

Blighty bound: UK recovery attracts EU citizens

The recovery in the UK economy has been drawing migrants back, with net migration to the UK reaching 260,000 in the year to June 2014. But the number of non-EU migrants coming to the UK has been declining, even as the number of people moving to the UK from other EU member states has been rising.

Educated and mobile: Skills are coveted

The battle is on to attract skilled migrants and it shows in the data. According to the OECD, the number of tertiary-educated migrants to its largely rich member countries has risen by 70 per cent in the past decade. Some 35m of the 115m migrants living in OECD member countries now have university degrees.

Cost concerns: Impact is broadly fiscally neutral

Opponents of rising migration say governments cannot afford the cost. Economists and business groups have long said the opposite is true: new arrivals do not just consume resources, they spend money and pay taxes. The OECD last year found that if there was a cost from new migrants it was generally small.

PD2: Nos está esperando, sabe que volveremos algún día, tiene toda la paciencia del mundo… Nos creo porque quiso. Pero nunca nos abandona y nos quiere junto a Él.