Han pedido a las autoridades locales que transfieran urgentemente todo el cash al Banco Central Griego… No hay más tesorería. Y como de coña, les van a pagar a los pobres ayuntamientos un 2,5% por este préstamo urgente. Te cagas lorito. Lo siguiente es un corralito, con empresas y particulares… No tienen para los pagos que deben:

Pero una cosa es el DEFAULT y otra distinta es la salida del euro GREXIT, que no tiene por qué ir de la mano…

Se acabó. ¿Habrá contagio en Italia, España, Portugal? Ese es el gran miedo… Ni lo dudes que lo habrá. La prima de riesgo de España ha dejado de estar en los 100 pb para irse a los 140 pb… Qué pereza, otra vez venga a hablar de la prima de riesgo!!!

Data from the Greek central bank, which records each euro that leaves the country as a liability, suggest the capital flight has reached unprecedented proportions. Over the six months through March, about 62 billion euros ($67 billion) were taken out of Greece. That's the equivalent of a quarter of the country's gross domestic product. Here's a chart:

It's hard to know when the exodus will end. Even if Greece and its creditors get past the current impasse, they will almost certainly have to start negotiations on a longer-term program to address a debt burden that, at more than 175 percent of GDP, remains far too large.

As Bloomberg View has argued, a better approach would be for Europe to focus on a final deal -- including significant debt relief -- that would quickly put Greece on a realistic trajectory toward solvency and economic recovery. The longer the bickering goes on, the more unnecessary damage will be done, eroding whatever benefits either side might hope to gain.

11 Acts Toward a Greek Tragedy

With negotiations faltering, the rhetoric intensifying and a daunting payment schedule ahead, there is mounting concern that the latest disagreements over Greece may be more than just another stage in the prolonged repeated game involving that country's debt drama.

The worry is that, this time, a ghastly set of circumstances is coming together to form an inevitable reality – that of Greece being ejected from the euro zone (a forced “Grexit”), which wouldn't be caused by a conscious decisions, but would be the result of a huge accident (“Graccident").

Here are the 11 things you need to know:

1. What is making this scenario seem more plausible is the simple fact that Greece is rapidly running out of money, a situation so dire that the unthinkable is on the table: a default on obligations to theInternational Monetary Fund, one of the world’s few preferred creditors.

2. With such an outcome becoming more than just thinkable, the walk away from Greek financial assets has turned into a jog that could be on the verge of turning into a run. Even some of the structural holders of Greek debt, such as foreign subsidiaries of Greek banks, have been exiting their holdings. Meanwhile, withdrawals of bank deposits are probably accelerating, this after large amounts have already fled the Greek banking system.

3. The result is to suck more oxygen from an economy that is already struggling mightily. It also worsens dependence on “emergency lending” from an already hesitant European Central Bank system, which misses no opportunity to say that such funding isn't intended to repeatedly fill gaps created by others -- especially because the ECB has been Greece’s only large official financier for quite a while.

4. The solution involves four main components: Policy reforms by Greece, immediate funding from creditors, additional debt reduction and easing some of the demands for budgetary austerity. These conditions will need to be implemented simultaneously, and should be accompanied by close collaboration and continuous constructive consultations among the Greek government, its European partner governments, regional institutions and the IMF. At the moment, what should be a cooperative undertaking is being approached uncooperatively.

5. While this is by no means the first dramatic moment of brinkmanship in the Greek crisis, the disagreements this time are much deeper and consequential. Dogma, morality and blind spots are playing a much greater role, obscuring economic and financial realities. Also, negotiations have been undermined by months of a public blame game, with accusations and counter-accusations (including some unusually personal ones).

6. Even though it has quite a bit of economic logic on its side, the new Greek government has failed both in meaningfully evolving the thinking of its creditors and in credibly signaling its commitment to carry out needed economic reforms. Part of this reflects unfortunate negotiating tactics, including public posturing in which nuances and confidence-building steps are lost in translation. But it also is the result of the intransigence of an impatient Europe, whose member states, to Greece’s detriment, no longer sort themselves along traditional debtor/creditor lines. That means the Greek government hasn’t even secured the negotiating backing of peripheral economies such as Ireland, Italy, Portugal and Spain.

7. Europe’s uncompromising stance reflects more than simply disapproval of the way the new Greek government has handled the negotiations. The continent is in a better place to deal with the potential collateral damage of a messy Greek situation, be it financial or technical, especially compared with 2010 and 2012. The euro group has taken major steps to counter the risk of contagion by establishing stronger regional arrangements to insulate members that could be more vulnerable (including Ireland, Italy, Portugal and Spain) from the dislocations in a particular country (in this case Greece). Markets have been much calmer, containing until now the pricing of extreme risk to Greek assets. Moreover, most of the peripheral countries have taken steps to increase their own defenses, especially compared with July 2012, when ECB President Mario Draghi's dramatic commitment to do “whatever it takes” averted the cascading financial collapse of several European economies (and the euro with them).

8. Being in a better relative position doesn't necessarily mean being totally safe. Fragile growth in Europe would probably take a hitfrom huge Greek dislocations. Some institutions would face financial pressures. And no one can forecast with any accuracy the regional implications of a potential Grexit/Graccident, given that these eventualities were never envisaged in the design of the euro zone.

9. Putting all this together leads me to postulate today a 45/10/45 probability distribution: There is a 45 percent chance that a last minute messy compromise allows the muddling-through to continue; a 10 percent chance that a meaningful policy breakthrough will be achieved, and a 45 percent chance that the outcome is a Graccident in which both the Greek government and its European partners lose control of the situation. Under this third scenario, a series of Greek payment defaults, bank runs and the imposition of capital controls would force Greece out of the single currency.

10. An optimist would espouse the 45 percent probability that a muddle-through compromise materializes at the 11th hour (or, to be more accurate, at 5 minutes to midnight). The realist would point out that there is a 90 percent chance that no decisive breakthrough is achieved, and that Greece and the euro zone experience an intensification of recurrent tensions and political stalemates, either immediately or down the road.

11. These probabilities aren't set in stone. They could -- and should -- be altered by more visionary policy making on both sides, along with early confidence-building steps. The challenge is that time to do so is running out.

Abrazos,

PD1: Según Paul Krugman:

Notes on Greece

OK, that was intense. I’ll write more about my visit, but right now (from Frankfurt, where I’m laying over for a couple of hours) I want to make a data point. about just how much adjustment Greece has done.

First, on the fiscal side, Greece has made an incredible adjustment — close to 20 percent of potential GDP, or the U.S. equivalent of about $3 trillion per year (not our usual 10-year calculation) in spending cuts and tax hikes:

CreditIMF

Second, Greece has accepted roughly a 25 percent cut in nominal private-sector labor costs, or more than 30 percent relative to the euro average, far more than anyone else:

CreditEurostat

You can make a pretty good case that the costs of this adjustment were so large that Greece would have been better off exiting the euro in 2010. You can make an even better case that Greece would have been much better off if it had never joined in the first place. But at this point these are sunk costs. If Greece can negotiate a halfway reasonable compromise, one that more or less pauses further austerity, it’s hard to see that the risks of exit would be worth it.

And the creditors would be equally well served by such a compromise.

So is it going to happen? Well, it’s the right thing to do — which tells you nothing.

PD2: En el gráfico he dibujado con datos de Eurostat el consumo público en Grecia y España desde 2001 en base 100 para ver su evolución y medir la intensidad del ajuste. Esta variable pesa aproximadamente el 20% del PIB y, si sumamos la inversión público, tendríamos la actividad total del estado.

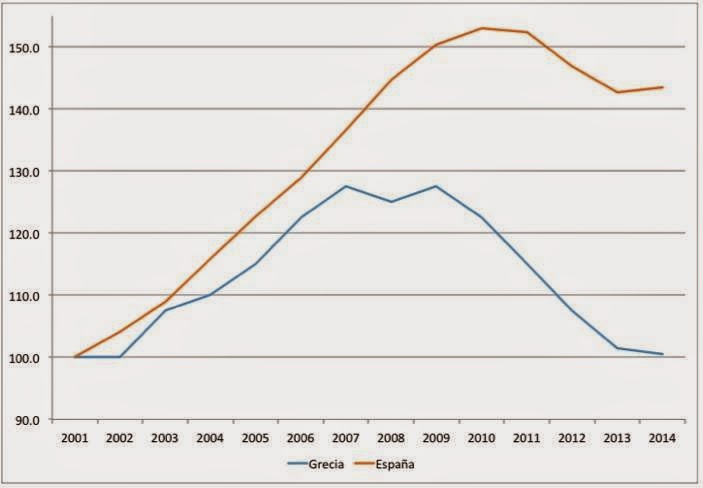

Se puede observar como en Grecia el ajuste de gasto fue mínimo en 2014 y, desde el verano, Grecia ya ha dejado de hacer ajuste fiscal. En España se ve cómo ha repuntado ligeramente el consumo público, por lo que en nuestro caso se puede afirmar que el ajuste fiscal acabó en 2013. Por eso las economías han vuelto a levantar el vuelo, aunque con una intensidad insuficiente para cerrar el agujero provocado por la depresión. Especialmente en Grecia.

Y el verdadero problema griego ha sido la cantidad de años que ha mantenido un déficit público abultado. Esto es insostenible…

PD3: El bono a tres años griego denota que es el fin:

En teoría lo iban a aguantar hasta el 9 de mayo que es cuando iban a reconocer que no podían pagar más…

Pero quizás no lleguen. Los siguientes pagos:

PD4: Culpa y ansiedad. No te eches la culpa de nada, el pasado, pasado está. Pídele perdón al ofendido, confiesa tus pecados y olvida. Y no tengas ansiedad por el futuro, no merece la pena. Dios proveerá