He empezado a leer sobre la posibilidad de que EEUU esté entrando en una recesión. ¿Sería esto posible?

Stock Performance Before, During & After Recessions

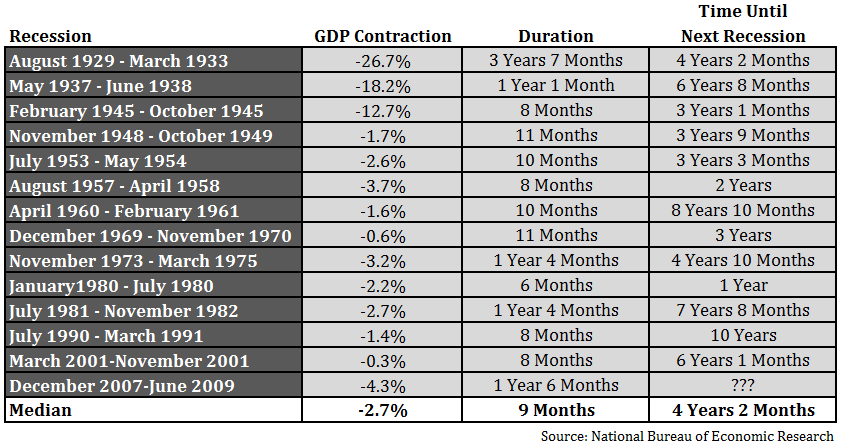

A few weeks ago I urged readers to get used to the fact that recessions are a fact of life that they need to get used to every 4-10 years or so. I shared the following table with each recession since the late-1920s:

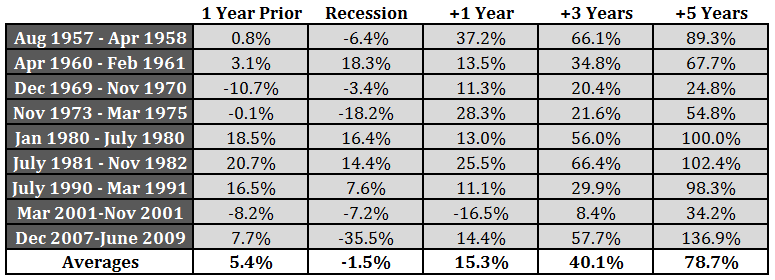

The next logical step from here is the see how stocks performed in and around these past recessions. I only have monthly S&P 500 returns going back to the mid-1950s, but that was good enough to show the total returns leading up to, during and after each of the past nine recessions:

This is another piece of evidence that shows why investing during periods of unrest usually pays off for investors. Three years out from a recession the annual returns showed an average annual gain of 11.9%. Five years out the average annual gain was 12.3%. Only one time since 1957 was the stock market down a year later following a recession, which occurred during the 2000-2002 bear market.

During the actual recessions themselves the total returns look much worse as they were negative, on average. But this average is made up of a wide range in results, as stocks have actually risen during 4 out of the last 9 recessions. And stocks were positive 6 out of the past 9 times in the year leading up to the start of a recession, dispelling the myth that the stock market always acts as a leading indicator of economic activity.

All of which is to say, what these numbers really tell us is that, in general, stocks tend to perform below average in the year leading up to and during a recession and perform above average in the 1, 3, and 5 years following the end of a recession (with the usual caveats that there are always outliers and this is a small sample size).

So all you have to do is figure out how to predict the next recession and you've got it made. Easy, right?

Brett Arends of MarketWatch (who himself was trying to figure out if we were already in a recession in late-2012) showed why it can be so difficult to predict recessions in real-time:

Remember the Great Recession that began in December, 2007? The economists at the National Bureau of Economic Research, who are basically the official scorekeepers of recessions, didn't discover the recession until December, 2008 – a year late, and only a few months before the episode (officially) ended.

The previous recession began in March, 2001 – but the NBER didn't call it a recession until November 26 of that year. By amazing coincidence, that was actually the month it ended (as they told us many months later).

The recession that began in July, 1990 wasn't called until April the following year. The recession that began in July, 1981 wasn't recognized until January of 1982. And so it goes.

We'll go into another recession at some point. There's a strong possibility that stocks could show underwhelming performance when it happens based on the strong gains U.S. stocks have shown over the past six year. Or maybe they'll fall before the business cycle slows. We'll see. Investor expectations are fickle.

Every market and business cycle is unique, as anyone who has been trying to handicap the current rally can attest to.

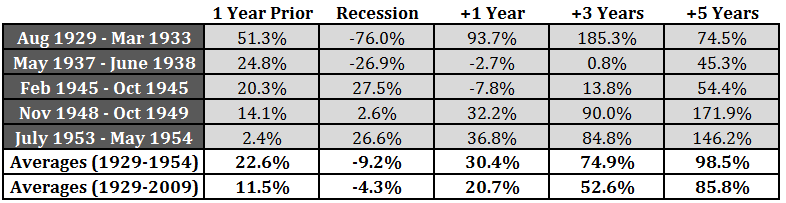

UPDATE: With a little help from Wes Gray at Alpha Architect I was able to put together the data set going all the way back to the Great Depression. Here are those results along with the averages over the entire period:

Mira lo que dicen estos:

The evidence is mounting...

While broadly-speaking, both 'hard' and 'soft' macro data has disappointed, as we noted previously, the scale of those 'missed expectations' is stunning - worst since Lehman. While this is blamed on weather, the fact is that America had 30% less snow this year than last and still, as the following charts strongly suggest, the YoY drops are on a scale that screams "recession"...

US Macro Data has surprised to the downside on a scale not seen since Lehman...

Retail Sales are weak - extremely weak. Retail Sales have not dropped this much YoY outside of a recession...

And if Retail Sales are weak, then Wholesalers are seeing sales plunge at a pace not seen outside of recession...

Which means Factory Orders are collapsing at a pace only seen in recession...

And Durable Goods New Orders are negative YoY once again - strongly indicative of a recessionary environment...

... oh, and core capital goods orders as well.

The last time durable goods orders fell this much, The Fed launched QE3 - indicating clearly why they desperately want to raise rates imminently... in order to have some non-ZIRP/NIRP ammo when the next recession hits.

And finally - coming full circle - it appears everyone is scrambling for credit to afford to maintain even a semblance of living standards (and lift retail sales) but "rejections" of credit requests have never - ever - been higher...

So the credit available to goose retail sales, which will goose wholesale sales which will drive factory orders... is no longer available to every muppet with a 500 FICO (old or new version) Score!!

But apart from that, given that US equities are at record highs, everything must be great in the US economy.

And just in case you figured that if domestic credit won't goose the economy, Chinese and Japanese stimulus means the rest of the world will save us... nope!! Export growth is now negative... as seen in the last 2 recessions.

And that's why America went to war...

{kind=link}

{kind=link}

{kind=link}

Abrazos,

PD1: Y les podría pillar a los bancos centrales con el pie cambiado, como otras veces ha ocurrido…

Strong currents that keep interest rates down

Central banks must move rates in an equilibrating direction — which they cannot choose

Why are interest rates so low? The best answer is that the advanced countries are still in a "managed depression". This malady is deep. It will not end soon.

One can identify three different respects in which interest rates on "safe" securities in the principal high-income monetary areas (the US, the eurozone, Japan and the UK) are exceptionally low. First, the short-term intervention rates of central banks are 0.5 per cent or lower. Second, yields on conventional long-term government bonds are extremely low: the German 30-year bond yields 0.7 per cent, the Japanese close to 1.5 per cent, the UK 2.4 per cent and the US 2.6 per cent. Finally, long-term real interest rates are minimal: UK index-linked 10-year gilts yield minus 0.7 per cent; US equivalents yield more, but still only plus 0.4 per cent.

If you had told people a decade ago that this would be today's reality, most would have concluded that you were mad. The only way for you to be right would be if demand, output and inflation were to be deeply depressed — and expected to remain so. Indeed, the fact that vigorous programmes of monetary stimulus have produced such meagre increases in output and inflation indicates just how weak economies now are.

Yet today we hear a different explanation for why interest rates are so low: it is the fault of monetary policy — and especially of quantitative easing, the purchase of long-term assets by central banks. Such "money printing" is deemed especially irresponsible.

As Ben Broadbent, deputy governor of the Bank of England, has argued, this critique makes little sense. If monetary policy had been irresponsibly loose for at least six years — let alone, as some have argued, since the early 2000s — one would surely have seen inflationary overheating, or at least rising inflation expectations. Moreover, central banks cannot set long-term rates wherever they wish. Empirical analysis of the impact of quantitative easing suggests it might have lowered bond yields by as much as a percentage point. But note that yields remained extremely low even well after QE ended, first in the UK and now in the US.

The price level is the economic variable that monetary policy influences most strongly. Central bankers cannot determine the level of real variables — such as output, employment, or even real interest rates (which measure the return on an asset after adjusting for inflation). This is especially true over the long run. Yet the slide in real interest rates is longstanding. As measured by index-linked gilts, they fell from about 4 per cent before 1997, to about 2 per cent between 1999 (after the Asian financial crisis) and 2007, and then towards zero (in the aftermath of the western financial crisis).

There is a more convincing story about why interest rates are so low. It is that the equilibrium real interest rate — crudely, the interest rate at which demand matches potential supply in the economy as a whole — has fallen, and that central bankers have responded by cutting the nominal rates they control. Lawrence Summers, former US Treasury secretary, has labelled the forces "secular stagnation" — by which is meant a tendency towards chronically deficient demand.

The most plausible explanation lies in a glut of savings and a dearth of good investment projects. These were accompanied by a pre-crisis rise in global current account imbalances and a post-crisis overhang of financial stresses and bad debt. The explosions in private credit seen before the crisis were how central banks sustained demand in a demand-deficient world. Without them, we would have seen something similar to today's malaise sooner.

Since the crisis, central banks have not chosen how to act — their hands have been forced. Events in the eurozone provide a powerful example. In early 2011, the European Central Bank raised its intervention rate from 1 to 1.5 per cent. This was wildly inappropriate, and in the end the ECB had to cut rates again and embark on QE. If central banks are to be a stabilising force, they have to move interest rates in an equilibrating direction — and that direction is not something they can choose.

Rising risk aversion might be another reason why real interest rates on safe securities have fallen. The idea is that the crises increased the appeal of the safest and most liquid assets. This is part of the explanation for ultra-low yields on German Bunds. But it does not seem to be the dominant explanation over the longer run. The gap between the interest rate on treasuries and US corporate bonds has not been consistently wider since the crisis, for example.

We should view central banks not as masters of the world economy, but as apes on a treadmill. They are able to balance demand with potential supply in high-income countries only by adopting ultra-easy policies that have destabilising consequences down the line.

When will we see an enduring rise in real and nominal interest rates? That would require a marked strengthening of investment, a marked fall in savings and a marked decline in risk aversion — all unlikely in the near future. China is slowing, which is likely to depress interest rates further. Many emerging economies are also weakening. The US recovery might not withstand significantly higher rates, particularly given the dollar's current strength. Debt also remains high in many economies.

Ultra-low interest rates are not a plot by central bankers. They are a consequence of contractionary forces in the world economy. While upward moves in rates seem ultimately inevitable from current levels, it is likely that historically low rates will be with us for quite a while. Those who bet on jumps in inflation and a bond-market rout will continue to be disappointed. The depression has been contained. But it is a depression, all the same.

PD2: Además, de lo que más se escribe es de la "secular stagnation"

Secular stagnation and capital flows

- can capital flows mitigate or even eliminate the problems generated by secular stagnation?

What's at stake: Former Chairman of the Federal Reserve and new blogger Ben Bernanke has generated many discussions this week by challenging the secular stagnation idea. Bernanke argues, in particular, that the stagnationists have failed to properly take into account how capital flows can mitigate or even eliminate the problems generated by secular stagnation at home.

The global secular stagnation hypothesis

Ben Bernanke writes that secular stagnation requires that the returns to capital investment be permanently low everywhere, not just in the home economy. All else equal, the availability of profitable capital investments anywhere in the world should help defeat secular stagnation at home. The foreign exchange value of the dollar is one channel through which this could work: If US households and firms invest abroad, the resulting outflows of financial capital would be expected to weaken the dollar, which in turn would promote US exports. Increased exports would raise production and employment at home, helping the economy reach full employment.

Ben Bernanke writes that many of the factors cited by secular stagnationists (such as slowing population growth) may be less relevant for other countries. Currently, many major economies are in cyclically weak positions, so that foreign investment opportunities for US households and firms are limited. But unless the whole world is in the grip of secular stagnation, at some point attractive investment opportunities abroad will reappear. If that's so, then any tendency to secular stagnation in the US alone should be mitigated or eliminated by foreign investment and trade.

Paul Krugman writes that international capital mobility makes a liquidity trap in just one country less likely, but it by no means rules that possibility out. You might think that you can't have a liquidity trap in just one country, as long as capital is mobile. As long as there are positive-return investments abroad, capital will flow out. This will drive down the value of the home currency, increasing net exports, and raising the Wicksellian natural rate. But this isn't right if the weakness in demand is perceived as temporary. For in that case the weakness of the home currency will also be seen as temporary: the further it falls, the faster investors will expect it to rise back to a "normal" level in the future. And this expected appreciation back toward normality will equalize expected returns after a decline in the home currency that is well short of being enough to raise the natural rate of interest all the way to its level abroad.

Tyler Cowen writes that it's the wrong comparison of interest rates and the wrong metric of expected currency appreciation. Rather than looking at real interest rate differentials, take the market's implied prediction for the euro to be the forward-futures exchange rates. These futures rates match the differences in nominal rates on each currency across the relevant time horizons. Those equilibrium relationships hold true with or without secular stagnation, whether in one country or in "n" countries, and from those relationships you cannot derive the claim that expected currency movements offset cross-border differences in real rates of return. The best way to speak of the non-ss countries, for international economics, is that their corporate sectors offer nominal expected rates of return which are relatively high, compared to their nominal government bond rates. Once you see this as the correct terminology, it is obvious that capital still will flow outwards to the non-ss countries, even with expected exchange rate movements.

Negative interest rates in theory and practice

Ben Bernanke writes that if the real interest rate were expected to be negative indefinitely, almost any investment is profitable. For example, at a negative (or even zero) interest rate, it would pay to level the Rocky Mountains to save even the small amount of fuel expended by trains and cars that currently must climb steep grades. It's therefore questionable that the economy's equilibrium real rate can really be negative for an extended period. Bernanke concedes that there are some counterarguments to this point; for example, because of credit risk or uncertainty, firms and households may have to pay positive interest rates to borrow even if the real return to safe assets is negative. Also, Eggertson and Mehrotra (2014) offers a model for how credit constraints can lead to persistent negative returns.

Larry Summers writes that negative real rates are a phenomenon that we observe in practice if not always in theory. The essence of secular stagnation is a chronic excess of saving over investment. Ben Bernanke grudgingly acknowledges that there are many theoretical mechanisms that could give rise to zero rates. To name a few: credit markets do not work perfectly, property rights are not secure over infinite horizons, property taxes that are explicit or implicit, liquidity service yields on debt, and investors with finite horizons.

Secular stagnation vs. global savings glut: the policy implications

Matt O'Brien writes that even though secular stagnation and the global saving glut are distinct economic stories, it's easy to confuse them since they look the same. Output is below potential and interest rates are low in both, which is just another way of saying that people want to save more than they want to invest. Secular stagnation says it's because there isn't enough demand for investment, while the global saving glut says, yes, it's because there's too much supply of savings. Now why does it matter which it is? Well, as Bernanke points out, different problems have different solutions. Secular stagnation means the economy is broken and the government needs to fix it by giving us more inflation and more infrastructure spending. But the global saving glut means the economy wouldn't need any fixing if governments would stop breaking it by manipulating their currencies down to run bigger and bigger surpluses and amass bigger and bigger piles of dollars.

Ben Bernanke writes that there is some similarity between the global saving glut and secular stagnation ideas. An important difference, however, is that stagnationists tend to attribute weakness in capital investment to fundamental factors, like slow population growth, the low capital needs of many new industries, and the declining relative price of capital. In contrast, with a few exceptions, the savings glut hypothesis attributes the excess of desired saving over desired investment to government policy decisions, such as the concerted efforts of the Asian EMEs to reduce borrowing and build international reserves after the Asian financial crisis of the late 1990s.

Ben Bernanke writes that of course, there are barriers to the international flow of capital or goods that may prevent profitable foreign investments from being made. But if that's so, then we should include the lowering or elimination of those barriers as a potentially useful antidote to secular stagnation in the US. Matt O'Brien writes that we used to have a global saving glut caused by other country's policy decisions, but now we have a global saving glut caused by other country's secular stagnation. If that's right, then it's not going to be enough to browbeat countries that aren't spending a lot into spending more.

Ryan Avent writes secular stagnation creates a dilemma. The ageing societies of the rich world want rapid income growth and low inflation and a decent return on safe investments and limited redistribution and low levels of immigration. Well you can't have all of that. The rich world could address the imbalance within its economies while simultaneously addressing the geographic imbalance by allowing much more immigration. Investing in people in developing countries in hard and risky. But if those people wanted to come to America and were allowed to, then lots of things change. Investing in those people would not then require that money be sent abroad, to a different financial system in a different currency overseen by a different government. If the savings are in rich countries and the most productive investments are in poor ones, then the savings can move or the investments can move

PD3: JP Morgan advierte que los tipos negativos en Europa van a ser solo puntuales…

Greenspan decía que las burbujas sólo se conocen cuando estallan. Sin desacreditar al expresidente de la Reserva Federal, siempre hay síntomas que pueden avisar de la existencia de una burbuja en un mercado concreto.

Cuando en 2006 España construía 760.000 viviendas (viviendas comenzadas a construir), tantas como Alemania, Italia y Reino Unido juntos, los indicios de la existencia de una burbuja en el mercado inmobiliario español eran evidentes. No obstante, siempre es difícil pronosticar hasta dónde se hincharán los precios en una burbuja y cuánto tiempo tardará en explotar. Mientras se sigue inflando la burbuja es complicado para los participantes en el sector mantenerse al margen. Retirarse del mercado anticipándose uno, dos o tres años al estallido de la burbuja y no participar de la fiesta durante ese periodo puede ser difícil de gestionar, sobre todo para las empresas cotizadas. Sus accionistas y los inversores en general entenderían, en el corto plazo, como un error mantenerse al margen mientras los precios siguen subiendo y las viviendas vendiéndose. Una vez estallada la burbuja reconocerán el éxito de la decisión previamente adoptada.

Analizando la burbuja inmobiliaria con perspectiva, es evidente que no podía durar un ritmo de construcción de viviendas superior a la suma de las construidas en varios países europeos con mayor población que España. Aun así, adivinar cuanto tiempo tardaría en estallar la burbuja era una incógnita.

Actualmente los síntomas de burbuja en el mercado de renta fija son evidentes. Aun así, cuánto tiempo transcurrirá hasta que dicha burbuja estalle es otra incógnita. El mercado de renta fija está intervenido por el Banco Central Europeo. Su actuación está distorsionando los precios y, en consecuencia, los tipos de interés ofrecidos por los emisores de renta fija.

Cuando estalle la burbuja de la renta fija, que estallará, comenzarán a oírse voces y análisis que mencionen la irracionalidad de la existencia de precios de las emisiones de renta fija que llevaron los tipos a negativos: pagar por prestar. Equivale a pagar a un inquilino por alquilarle una casa. En el corto plazo todo se puede explicar, pero la situación actual de la renta fija es totalmente insostenible en el medio plazo. El BCE no estará interviniendo de forma permanente en el mercado comprando bonos. La Reserva Federal compró bonos durante seis años, pero tras dicho periodo ha dejado de comprar y no tardará en subir los tipos de interés de los Fed Funds, lo que se traducirá en una subida de tipos en la práctica totalidad de los bonos soberanos norteamericanos.

En Europa el BCE lleva escasamente un mes comprando de forma intensiva bonos en el mercado (60.000 millones de euros). Su plan inicial es adquirir bonos hasta septiembre de 2016 pero dependerá de la evolución de la inflación y de las expectativas inflacionistas. Si la inflación subiera con anterioridad a dicha fecha, el BCE recortaría el ritmo de compra actual, o incluso dejaría de intervenir. Por otro lado, si la inflación y las expectativas de inflación continuaran sin repuntar, el programa de compra de bonos podría prolongarse, pero es evidente que antes o después finalizará. Cuando esto ocurra, los tipos de interés de los bonos subirán y el estallido de la burbuja de la renta fija será inevitable, si es que no ha estallado con anterioridad.

Lo mismo que ahora en 2015 cualquiera se pregunta cómo es posible que en 2006 pocas voces advertían de la existencia de una burbuja en el sector inmobiliario dadas las señales que daban las cifras de construcción de viviendas en España comparado con nuestros vecinos europeos, dentro de unos cuantos años se preguntarán que cómo es posible que no existiese en 2015 una alarma general por la existencia de una enorme burbuja en la renta fija. Los tipos de interés negativos son una muestra indudable de ello, aunque puedan prolongarse en el tiempo.

La inmensa mayoría de los participantes en el mercado de renta fija parecen no percatarse de la existencia de la burbuja existente en este mercado. O bien, intuyendo su existencia se ven forzados a participar en la "fiesta" mientras la música siga sonando. Pocos son capaces de abandonar la fiesta antes de que acabe. Las consecuencias de no retirarse a tiempo son dolorosas

PD4: ¿No les pasará a los estadounidenses que les toque ahora sus 394 semanas de purga?

Y mientras, se atrasan las expectativas de una subida de tipos por parte de la FED hasta el primer trimestre:

PD5: Mira qué bueno el Papa celebrando su santo la semana pasada con los trabajadores del Vaticano:

Con qué carita le miraban los de enfrente!