La bolsa china ha vuelto a estar muy floja estos días por culpa de lo mismo que ocurrió en agosto: sentimiento que va a crecer menos su PIB, junto con un deslizamiento del yuan. Y sin embargo, no veo motivo de alarma porque las causas no son suficientes para que debamos cambiar la estrategia a largo plazo.

Evolución del yuan: Entró muy débil, en los 8,3 yuanes por dólar en la OMC, en 1999. Se le estuvo pidiendo por parte de EEUU que se apreciara y lo hizo pasando de los 8,3 hasta los 6 yuanes/dólar. Y se ha depreciado hasta los 6,57 actuales:

La bolsa de Shangai: Ha estado lateral durante muchos años, mientras su economía se doblaba en tamaño (es más difícil crecer a una tasa del 7% cuando eres tan grande, que a una tasa del 10% cuando eres mucho menor),

y sus empresas ganaron muchos beneficios. Y después de la fallida subida de 2015, ha vuelto a donde estaba antes.

Mientras que otros mercados han estado subiendo mucho en estos años…

Donde invertimos nosotros, la bolsa de Hong Kong a través del índice ^HSCE, la subida fue más modesta, y lo ha perdido lo ganado. El mercado es el más barato del mundo, con un PER de 6,9 veces beneficios. Saldrá de esta larga lateralidad en cuanto la presión de los medios se tranquilice.

Las acciones H (las del HSCE) cotizan con un descuento del 38% frente a las acciones A de Shangai, lo que provoca un soporte a caídas adicionales.

Desde el punto de vista macro, los datos no son tan negativos. Ya sabes que está habiendo un cambio de modelo, de producción a consumo. Mira el PMI de ambos:

No está mal:

Más datos de China con mayor perspectiva:

Exportaciones: (dato de ayer)

Nos hemos vuelto a los niveles del cierre de agosto pasado. Se ha completado de forma triangular la subida de mitad de año 2015 con la bajada posterior. No creo que haya motivo de alarma, sino que pensando a largo plazo, acabará por salir de esta larga fase lateral que hemos vivido…

China es un mercado muy grande, con muchos consumidores que van a comprar de todo, con una gran capacidad de ahorro, con una gran capacidad de sobrevivir a una fase muy floja de las economías occidentales. El mundo desarrollado vive todavía una época de grandes excesos, coletazos de la enorme crisis de 2008, un endeudamiento no resuelto, unas políticas monetarias que dan poco pie a hacer más (tipos cero actuales y paquetes desorbitados de estímulo que no se pueden repetir). Esa es la alternativa, y a pesar de la aparente debilidad de las bolsas a corto plazo, es posible que sea lo más seguro ante eventos imprevistos. Un abrazo

PD1: Desde Franklin Templeton dicen:

China's Conundrum

New-year celebrations in the Western world gave way to concerns about China as its stock market opened 2016 with a loss, triggering declines in equity markets globally. The 7% decline in China's domestic A-share market on January 4 was enough to trigger China's new circuit-breaker system, halting transactions on the first day of trading in the new year and prompting government intervention to prop up stocks.

Retail investors were certainly involved in the selling but also large shareholders, particularly top company executives who hold shares in their own companies. This is why the Chinese government has put restrictions on the amount they can sell. To ease the panic in the market, China's securities regulator (the China Securities Regulatory Commission) just announced a cap on the size of stakes that major investors would be allowed to sell to only 1% of a company's shares. This would be effective for three months starting on January 9. The entire psychology of the market has not been good for a few reasons, one being the decline of China's currency, the renminbi (RMB), which has prompted investors to exit RMB-denominated assets such as Chinese-listed shares, and also because of the fear that the Federal Reserve's decision to raise rates in the United States could negatively impact other economies. There is still some uncertainty about further rate changes ahead but the current expectation is that US interest rates may even go higher.

Clearly, many investors are worried right now. As we see it, there is no question that China should continue to have strong growth this year, but one might say China is facing a bit of a conundrum. On the one hand, the government wants stability, but on the other, it also is striving toward more openness. That means we could see more volatility in China's market this year as these conflicting forces play out.

It's important to remember that China's economy is a planned economy, something that I think has been overlooked by many people when they ponder the possibility of bank failures, overleverage and other worst-case economic scenarios. At the end of the day, the Communist party (the state) is determining the direction of the economy and, in our view, has the wherewithal to take measures it feels are needed to further its goals. However, going forward it will be difficult for China's government to maintain control if the goal is for a more open economy. The writing is on the wall in the sense that China aims to free the economy and particularly the RMB. This will likely be done in stages, very gradually, to help promote the desire for stability. I think it's important for anyone interested in understanding China's goals—and the potential market implications—to read the 10 points of the plenum, which outline the direction of the economy. Some industries will be reorganized; some will be de-emphasized. But the country's direction seems clear to us—toward a more open economy, a more market-oriented economy that adjusts to international movements of capital with the RMB not only a reserve currency, but a major international trading currency.

We think the type of market volatility we have seen will likely continue this year, and not only in China. Volatility is increasing in many markets and it's something investors will likely need to learn to live with. We view periods of heightened volatility with the lens of potential investment opportunities—allowing us to pick up shares we feel have been unduly punished. But we understand these types of conditions are difficult for people who are afraid of volatility. In the case of China, the government's efforts to maintain stability on the one hand and to allow a freer market on the other is a difficult balance to achieve.

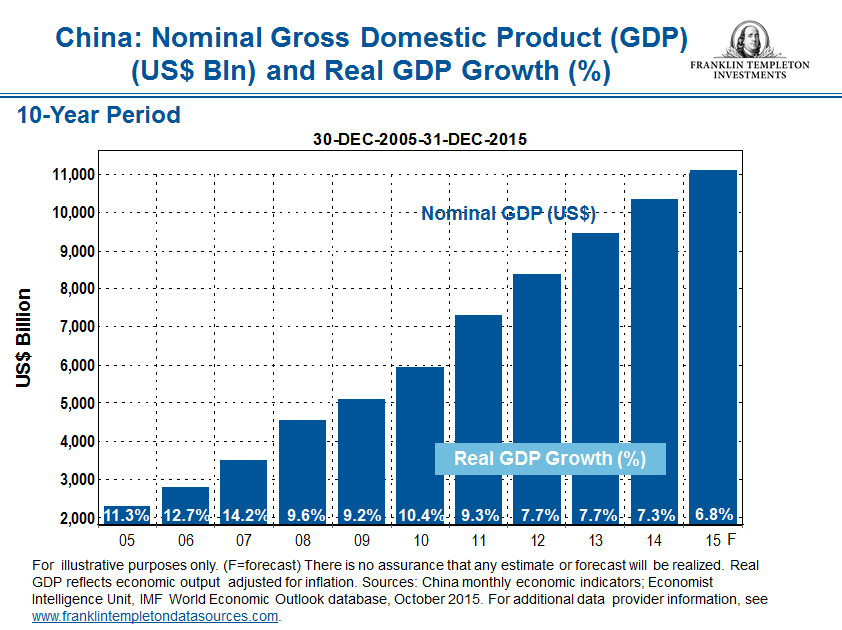

That said, we are not terribly concerned about growth in China, nor its long-term investment prospects. We would dub current 2016 projections of about 6% in gross domestic product growth1 as quite strong given that the size of the economy has grown tremendously in dollar terms from that of a few years ago, when growth rates were stronger but with a smaller base. This is another aspect we think many investors may be missing when they see growth slowing. (See chart below.) The fundamentals in China are still excellent, in our view. It is one of the fastest-growing economies in the world even if the growth rate has decelerated.

{kind=link}

We continue to look for investment opportunities in China, and are confident in the long-term growth story we see there in light of a planned shift in its economy from an export-oriented model to a more domestic-focused one. China is also going through a dramatic transition from a rural society to an urban society. For a more in-depth look at the structural and economic changes taking place in China, I encourage you to check out "China: Searching for a New Equilibrium" by my colleague Michael Hasenstab, CIO of Templeton Global Macro. US investors can view it here. Investors outside the United States can view it here.

PD2: El petróleo de nuevo desplomado hasta unos niveles hace muchos años no vistos, por debajo de los 30 dólares:

Quizás hemos sido engañados por los altos precios durante tantos años. El aumento de la producción y la menor demanda actual, hace que quizás lo tengamos muchos años a estos niveles. Es mejor, digo yo.

Hay países que no opinan lo mismo:

Y otros que no salen: Noruega, Canadá, EEUU con su frackling… Les va a doler estos precios…, un montón.

A los países importadores de crudo (España, China…), no. España consume 475 millones de barriles al año, la bajada de ayer supone un ahorro versus 2012/13/14 de 25.000 millones de euros, o 600€ por español. ¿Cuándo me los van a dar que paso a cobrarlos?

PD3: David Bowie era un tipo peculiar. Se convirtió y era muy espiritual, hasta el punto que en uno de sus conciertos multitudinarios en Wembley (Londres), rezó un Padrenuestro de rodillas por su amigo Freddy Mercury, cantante de Queen, que acababa de fallecer: https://www.youtube.com/watch?v=ANQspcmfhJU ¿Y la vergüenza de expresar la fe? Ninguna…