Crecer sí que es importante, ya que el crecimiento es condición necesaria, aunque no suficiente, para salir de la crisis de deuda. Hay que desaparcar lo comprado por la FED, y eso generará problemas a futuro. La política fiscal que va a emprender Trump es otra buena patada hacia adelante, pero no olvides que seguimos inmersos en una grave crisis de deuda…:

Goldman Sachs is relatively optimistic about growth in 2017, for three reasons: first, despite the lack of spare capacity, US recession risk remains below the historical average; second, financial conditions should remain a growth tailwind - at least in the first half of 2017; and third, we expect a fiscal easing accumulating to 1% of GDP by 2018. However, uncertainty remains and here is what Jan Hatzius and his team believe are the ten most important questions for 2017.

1. Will growth remain above trend?

Yes. Admittedly, the expansion is quite advanced. It has already lasted about 18 months longer than the median completed expansion since the mid-1800s. And while expansions do not die of old age, history shows that they are at greater risk when spare capacity is exhausted, as it probably is now. So it is especially important to monitor whether growth may be running out of steam.

Nevertheless, we are relatively optimistic about growth in 2017 and expect real GDP to climb at a 2.2% rate. First, despite the lack of spare capacity, US recession risk remains below the historical average, as shown in Exhibit 1. The most important recession predictors, at horizons longer than the next few quarters, are spare capacity and past credit growth. Spare capacity has dwindled, which has boosted the recession probability somewhat, but output is not yet meaningfully above potential. Moreover, debt growth has been very moderate in the economy as a whole, despite pockets in the corporate sector where the credit cycle is more advanced. This is also consistent with alternative measures of financial imbalances such as the private sector financial balance, which remains comfortably in surplus to the tune of 2½% of GDP.

Exhibit 1: US Recession Risk Below Historical Average

Source: Goldman Sachs Global Investment Research

Second, financial conditions have turned from a growth headwind into a growth tailwind over the past year, as shown in Exhibit 2. Admittedly, financial conditions have tightened modestly in recent months as the increase in bond yields and the appreciation of the US dollar have outweighed the rally in the equity market. But our analysis shows that, in practice, the growth impulse depends on the year-to-year change in our financial conditions index, at least to a first approximation. Barring a big tightening in coming months, the impulse should therefore remain quite supportive, at least in the first half of 2017.

Exhibit 2: FCI Impulse Likely to Remain Positive for Much of 2017

Source: Goldman Sachs Global Investment Research

Third, by the time the financial conditions impulse diminishes in the second half of 2017, fiscal policy should begin to turn more supportive. We expect a fiscal easing of about 1% of GDP once it is fully phased in, consisting mostly of personal and corporate tax cuts. Although the multiplier associated with these cuts is probably relatively small—we estimate an average of 0.6 across the entire assumed fiscal package—they should nevertheless make a respectable contribution to growth in the second half of 2017 and first half of 2018, as shown in Exhibit 3.

Exhibit 3: A Fiscal Boost to Growth

Source: Department of Commerce. Congressional Budget Office. Goldman Sachs Global Investment Research.

2. Will the incoming administration enact major tax-related legislation?

Yes. Some type of tax legislation seems very likely to pass in 2017, for three reasons. First, Republicans have it in their ability to pass tax legislation without Democratic votes, by using the reconciliation process. Second, tax reform—or at least a tax cut—was an important aspect of the presidential campaign. Third, it has been a top priority for congressional Republicans, and particularly House Speaker Paul Ryan, for several years.

Congressional Republicans appear to be primarily focused on corporate tax reform, with a particular focus on lowering the statutory rate and reforming the treatment of cross-border income (see here for more detail). We believe the principal goals among many lawmakers are to lower the effective tax rate on business investment and to reduce the incentive for US companies to locate production overseas and/or to redomicile via “inversion” transactions. The most controversial item in the House Republican tax reform plan appears to be the destination-based border-adjusted corporate tax. If enacted, this would have important implications for importers and exporters, domestic price inflation, and the value of the dollar. We see a 30% probability that this proposal is included in whatever tax reform legislation Congress ultimately enacts next year.

Reductions in individual income tax rates also appear likely. The existing plan from House Republicans cuts the top marginal tax rate to 33% from 39.6%, and reduces the number of tax brackets from seven to three. The proposal also calls for repealing the Affordable Care Act (ACA, or “Obamacare”), including its taxes on investment income and higher-income earners, and would make a number of other reforms to the individual income tax code. Analysis by the Tax Policy Center suggests the plan would reduce federal government revenue by about $2 trillion over ten years.

Exhibit 4: Comparing Tax Plans

Source: Office of Management and Budget. House Ways and Means Committee. Trump Campaign. Goldman Sachs Global Investment Research.

3. Will the housing recovery continue?

Yes, at a moderate pace. Admittedly, the 80bp increase in 30-year fixed mortgage rates since September has complicated the housing outlook somewhat. Our analysis shows that this could take as much as 5% off the level of housing starts in the next few quarters, relative to a baseline without mortgage rate shocks (Exhibit 5).

Exhibit 5: Higher Mortgage Rates Likely to Weigh on Residential Investment

Source: Goldman Sachs Global Investment Research

But the positive forces underpinning the housing recovery remain substantial. From a short-term perspective, it is noteworthy how strong the demand indicators have looked recently—new single-family home sales are up about 20% year-on-year and the homebuilders’ index hit an 11-year high in December. And more fundamentally, the still-low level of housing starts relative to the underlying demographics should continue to provide support in coming years. Exhibit 6 shows that the sum of the demographic trend in household formation and demolitions is currently about 1.4 million per year—above the current level of housing starts of around 1.2 million.

Exhibit 6: Housing Starts Remain Below Demographic Trend

Source: Department of Commerce. Goldman Sachs Global Investment Research.

4. Will consumption continue to outperform capital spending?

No. Growth has been quite unbalanced over the last two years. Since the third quarter of 2014, real personal consumption has grown 3% (annualized), more than 1pp above the economy’s estimated long-term trend of 1¾%. In contrast, real business investment has stagnated. Outside early recovery episodes, when consumption often leads capital spending, such a gap is quite unusual. We expect it to close because much of it is a one-off effect of the 2014-2016 decline in energy prices.

The energy price decline sharply boosted real household income, and thereby consumption. As shown in the left panel of Exhibit 7, lower energy prices added about 0.6pp to the annualized growth rate of real disposable income over the past two years. The marginal propensity to consume out of energy-related changes in real income is usually thought to be relatively high because lower- and middle-income households typically spend a larger share of their income on energy than higher-income households. This suggests that most of this 0.6pp boost probably translated into stronger consumption growth. But most of it is now likely behind us.

Conversely, the energy price decline sharply hit corporate profits, and thereby capital spending. The right panel of Exhibit 7 shows that losses in the oil & gas industry subtracted about 15pp from corporate profit growth over the course of 2015. Now the weakness is behind us, and corporate profits are once again growing at a reasonable pace.

Exhibit 7: Energy Price Declines Lifted Household Income but Weighed on Profits

Source: Department of Commerce. Department of Labor. Standard and Poors. Goldman Sachs Global Investment Research.

5. Will the labor market overheat?

Yes, slightly. The starting point at the end of 2016 is approximately full employment. Some indicators such as the broad underemployment rate U6 and summary measures of nominal wage growth still show a small amount of labor market slack. Others such as the job openings rate and the level of skill shortages are already consistent with a modest amount of labor market overheating.

Our growth forecast for 2017 implies that the economy will grow about ½pp above its longer-term trend rate and as much as 1pp above the pace that has been consistent with stable labor market slack in recent years. If so, we would expect the unemployment rate to fall ¼-½ pp over the next year, with other labor market indicators following suit. This would imply a small amount of labor market overheating.

Labor market overheating must eventually be reversed to keep inflation from rising too far above the target. But reversing an overheating means that the unemployment rate would need to rise, and it has historically been very difficult to do this without pushing the economy into recession. In fact, as shown in Exhibit 8, there has never been a rise in the US unemployment rate of more than ?pp that was not associated with a recession. Outside the US, there are precedents for such "soft landings from below" (see here), but the point that these are difficult to achieve holds more broadly.

Exhibit 8: A Soft Landing from Below Is Difficult

Source: Department of Labor. NBER.

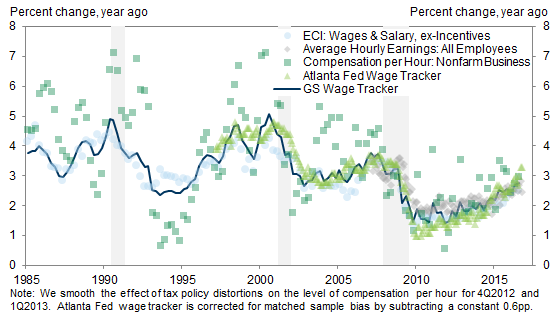

6. Will wage growth hit our 3.0%-3.5% estimate of its full employment level?

Yes. Wage growth has accelerated meaningfully in recent years as the labor market has tightened (Exhibit 9). The firming has been most pronounced at the bottom end of the wage distribution, aided by minimum wage hikes at the state and city level that are likely to continue in coming years—even if an increase at the federal level now appears very unlikely. While aggregate wage growth remains somewhat below both the pre-recession rate and the equilibrium rate that we would expect in a full employment economy, we do not see this as a sign that hidden slack remains. Rather, a combination of the impact of past slack earlier in the year, negative composition effects on aggregate wage growth, and an environment of weak productivity growth and soft inflation appear to account for most of that gap (see here for more detail). As the labor market tightens further wage growth should continue to firm.

Exhibit 9: Wage Growth Continues to Accelerate

Source: Goldman Sachs Global Investment Research

7. Will inflation reach the Fed’s 2% target?

Yes. Headline PCE inflation has picked up from a low of 0.2% year-over-year in September 2015 to 1.4% as of last month. If energy prices hold around the current level, PCE inflation should reach the Fed’s 2% target by February or March. Core PCE inflation has also firmed over the last year, rising from a low of 1.3% to 1.6% as of November. We expect core inflation to continue accelerating—reaching 2% by Q4—as the labor market tightens further and the lagged effects of past dollar appreciation fade.

We will be keeping a particularly close eye on medical care inflation next year, which has been the main factor behind the divergence between core CPI and core PCE inflation recently. As we have discussed in detail elsewhere, only about half of the gap between the two measures can be explained by differences in scope. The remaining difference between the two series largely reflects measurement error, in our view, with the CPI overstating reimbursement rate inflation and the PCE index understating it. We therefore expect the two series to converge over time, giving a lift to core PCE inflation while holding core CPI inflation roughly steady in 2017.

8. Will the Fed hike faster than implied by market pricing?

Yes. At present markets are discounting an end-2017 federal funds rate of about 1.2%—54 basis points (bp) above the current effective funds rate, and implying just over two 25bp rate hikes for the year. We continue to expect the FOMC to raise rates three times, with the first hike coming in June. At the end of October markets were pricing in about 30bp of rate increases for 2017—slightly more than one 25bp rate hike—so the gap between market pricing and our forecast has already narrowed quite a bit, but we still think market pricing looks too low. Much will depend on the incoming data early in the year and the evolving prospects for fiscal stimulus. If growth momentum continues to look solid and fiscal stimulus appears likely, we would expect most FOMC members to support picking up the pace of hiking.

9. Will the market’s terminal funds rate estimate continue to rise?

Yes. In our annual questions for 2016 we said the same, but decided the verdict was inconclusive (see here for our review). Forward OIS rates declined for much of 2016, but increased sharply after September (Exhibit 10). Markets are now pricing a terminal funds rate of 2.5%—virtually identical to the level at the end of 2015, but up more than 100bp from the 2016 lows.[1]

Even after the latest increase these estimates still strike us as quite low. The US economy is close to full employment, growing above trend, and generating inflation around 2%. Plus, markets already see the funds rate reaching 1.2% by the end of next year. Given this economic backdrop and with the prospect of more rate increases over the near-term, market pricing for the terminal funds rate seems unsustainable. Moreover, our research shows that one key tenet of the depressed r* narrative rests on relatively shaky empirical ground: historical evidence suggests market participants and Fed officials may be assuming too tight a link between potential growth and equilibrium policy rates (see here for details).

Exhibit 10: Only a Partial Recovery in the Market’s Terminal Funds Rate Estimate So Far

Source: Goldman Sachs Global Investment Research

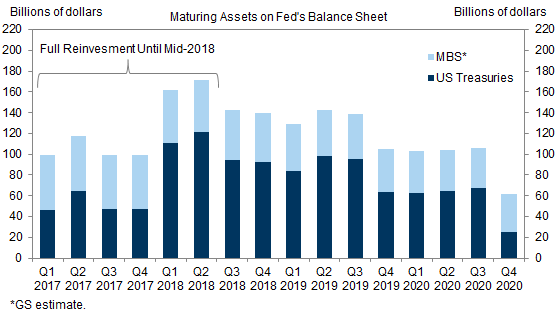

10. Will the Fed start to shrink its balance sheet?

No. Fed officials have said that the size of the central bank’s balance sheet will likely remain unchanged until funds rate increases are “well under way”. We have interpreted this guidance to mean that full reinvestments in the Fed’s securities portfolio would continue until mid-2018, when we expect the funds rate to be around 2% (Exhibit 11). After that we forecast that policymakers would begin a slow, tapered runoff of the balance sheet that would last for several years.

Exhibit 11: We Expect the Fed’s Balance Sheet to Remain at Current Size in 2017

Source: Federal Reserve. Goldman Sachs Global Investment Research.

Some of the economic advisers to President-elect Trump appear to favor a smaller Fed balance sheet with a shorter duration, and this issue could come up in any nomination hearings for the two open Board positions. However, we do not think the election result meaningfully affects the outlook for the balance sheet for 2017. First, Chair Yellen will remain at the helm until early 2018, and will likely continue to execute the committee’s current plans—even with the addition of a few President-elect Trump appointees to the Board. Second, in our view, the ideal size of the central bank’s balance sheet is not really a macroeconomic issue—rather, most of the key determinants are institutional and regulatory matters (see here). As a result, the views of the new administration may evolve as it begins to tackle regulatory reform and debt management concerns.

Y estas son sus conclusiones del crecimiento económico a futuro:

Y lo que digo yo es que sí, con la política fiscal de Trump, el crecimiento será mayor, del 4% anual en los primeros dos años. Lo malo es que los mercados han sobre descontado ya parte de este efecto y las previsiones de beneficios no son tan boyantes, por lo que es probable que dure este tirón hasta la primera parte del año, a lo sumo, y acabe en niveles parecidos a los actuales. Hay potencial, pero se vislumbran muchos riesgos que hagan que la euforia actual se trunque por ir viendo políticas incumplidas o de efectos no tan buenos como se esperan. Abrazos,

PD1: Segundo propósito de Año Nuevo: No criticar, no hablar nunca mal de nadie. Cada uno es como es y no tenemos por qué hablar mal de la gente porque no nos guste lo que hacen, porque no sean como nosotros… Cuando juzgamos a los demás, les estamos odiando y estamos aquí para querer hasta a nuestros enemigos…