Las caídas del mercado de bonos en todas partes, descontando un escenario de mayor inflación, puede que estén injustificadas y ésta no llegue tan pronto:

Esta es la expectativa de inflación dentro de 5 años:

Y la europea:

Trumpflation: Not Now, Maybe Later

Strong early reactions in the bond market to stimulus plan miss the bigger picture

The bond market is a binary creature: It sees every event as either inflationary or deflationary. It has quickly concluded that Donald Trump's shock victory is the former. Since then the 10-year Treasury yield has leapt a third of a percentage point, about half of that because of higher expected inflation.

This is an overreaction. Presidents and policies make U-turns; inflation and economic growth don't. The U.S. and the world have been stuck in a low-growth, low-interest rate rut since 2009, and Mr. Trump's policies can at best change that at the margin.

That said, Mr. Trump's election is part of a rising tide of global populism, a phenomenon that in the past has usually brought inflation—a risk for a later date.

At first blush, Mr. Trump looks like he will usher in a new era of fiscal profligacy that will flood the world with new debt to absorb. He has proposed a tax cut that several outside analysts say would add about $6 trillion to deficits in the coming decade and spending hundreds of billions of dollars via tax credits on new infrastructure.

That's a lot, but then the world has a structural surplus of savings and a shortage of investment. This year, the euro area, China and Japan will run surpluses on their current accounts—the balance on all trade and investment income—of roughly $850 billion. In short, the bonds needed to finance Mr. Trump's deficits will find ready buyers.

The actual deficit impact is likely to be much smaller. Mr. Trump doesn't appear wedded to any specific numbers. Kevin Brady, Republican chairman of the House of Representatives' tax-writing committee, said Tuesday the tax overhaul would aim not to raise the deficit. The growth impact is also likely to be modest. The bulk of the tax cuts will likely go to corporations and the wealthy, whose spending doesn't vary much with their tax bills. Lower corporate tax rates should encourage investment and growth but the impact would be uncertain and gradual.

Macroeconomic Advisers estimates a $4 trillion tax cut along the lines of Mr. Trump's proposal would boost growth just 0.2 percentage point over the next three years. On infrastructure, Mr. Trump will encounter the same awkward reality that PresidentBarack Obama did seven years ago: There aren't many shovel-ready projects.

Unlike in 2009, this fiscal stimulus will be hitting when the economy is close to full employment with far less spare capacity. Yet it's premature to assume inflation will therefore jump. In the last decade inflation, excluding swings due to energy, has proven surprisingly inertial, barely moving in response to high unemployment. The same is likely true if unemployment drops further below its "natural" level.

This will shape how the Federal Reserve responds. "I don't think we should say, even if there's going to be fiscal stimulus, we know that will translate into such-and-such an increase in inflation," Fed governor Dan Tarullo said Tuesday.

To be sure, fiscal stimulus will likely hasten the Fed's process of raising rates, but it's less likely to change the end point. In the long run, rates are being held down by structural factors such as aging population and slow productivity growth.

Mr. Trump's anti-globalization policies could bolster inflation. Goldman Sachs estimates that tariffs of 35% to 45% on Mexican and Chinese imports, as Mr. Trump has threatened, would add 0.2 percentage point to inflation while deporting 2.5 million illegal immigrants, by restricting the supply of labor, would add up to another 0.1 point.

But will Trump go that far? Though clearly a protectionist, Mr. Trump and his advisers have often described the threat of tariffs foremost as leverage to extract concessions rather than prelude to a trade war. His deportation threats have changed repeatedly.

And while restricting immigration and trade will hurt productivity, which raises costs, lower corporate tax rates and regulation should work in the opposite direction by bolstering investment.

Still, dissecting Mr. Trump's policies misses the bigger picture. He's the latest in a global wave of populists toppling the established political order with its appeals to disaffected working-class voters.

In emerging markets, populist leaders often presided over an initial economic boom fueled by easy fiscal and monetary policy; inflation and crisis usually followed. The U.S., of course, has much stronger institutions, including an independent Federal Reserve. And Republicans in Congress have been harshly critical of what they consider overly easy monetary policy and want to subject its monetary decisions to congressional audit.

But with one of their own in the White House, Republicans in Congress may worry less about inflation and deficits. Half a century ago, inflation began to climb when supposedly independent Fed chairmen succumbed to political pressure, first under Lyndon Johnson and then under Richard Nixon. If Congress curbs the independence of the Fed now, it may inadvertently ease the way for inflation's return down the road.

Y lo mismo puede pasar con la debilidad de todas las divisas contra el dólar… Esa fortaleza aparente del dólar estos días, puede ser agua de borrajas. No hay más que ver lo que le pasó a la libra tras el Brexit…: se calmó y rebotó. Lo mismo que le pasaron a las divisas emergentes durante el año pasado y el arranque de este: perdieron y recuperaron parte de lo que habían bajado…

La realidad ahora es apabullante. Varapalo en el mercado de bonos desde las elecciones Usa, haciendo que el spread entre el bono alemán y el estadounidense a 10 años haya alcanzado su máximo desde 1989:

¿Qué sentido tiene? Ninguno. Y eso que el bono alemán arrastra a los demás bonos europeos hacia abajo. Sí, ya sé que en Europa estamos comprando, en teoría hasta marzo 2017, la burrada de 80.000 millones de euros al mes en nuestro QE, pero, ¿Qué sentido tiene que los bonos español o italiano tengan una rentabilidad menor a los yanquis? Ninguno.

Quizás está tan pasado que deberían subir los bonos europeos de rentabilidad hasta unos niveles más razonables:

O al menos eso dicen estos, que argumentan que si no ocurre esto:

Tendrán problemas la FED, los tenedores de bonos, la forma de financiar el déficit por cuenta corriente USA… Quizás esto solo sea un envite especulativo del mercado y todo vuelva a su cauce previo…

Con esta curva de tipos y con esta reciente subida brutal hacia arriba:

Las consecuencias son para el dólar que se fortalece, alcanzando los 1,06 euros/dólar, y lo que te rondaré morena, que ya se habla de llegar a la paridad… El problema es que los bancos centrales van a salir para tratar de parar este desaguisado de rentabilidades al alza y de fortaleza del dólar y no tienen apenas herramientas para hacer casi nada. Ya no valen las palabras de "haré todo lo que pueda…", ahora verán en sus carnes lo que es palmar…

Lo único que te hace dudar es la solvencia de muchos países, la solvencia de EEUU:

Y de otros muchos europeos:

Es que seguimos sufriendo una grave crisis de deuda, que parece olvidamos y tal…, de la que no se sale emitiendo más deuda!!! Abrazos,

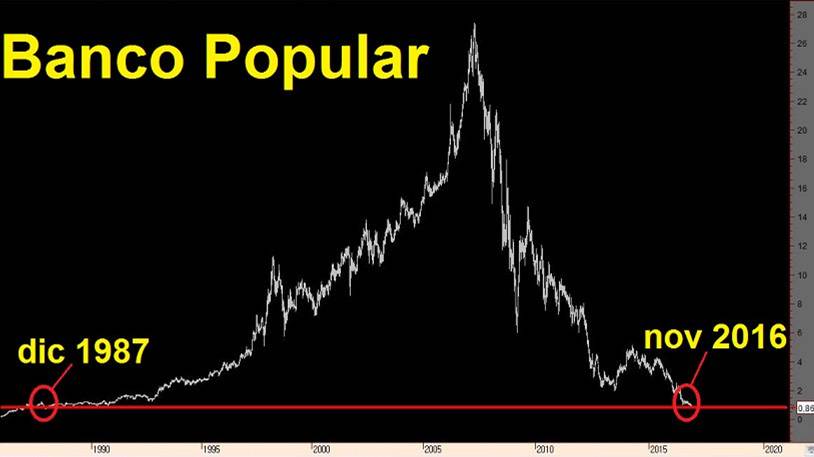

PD1: Por cierto, el Banco Popular español no aguanta y se sigue desmoronando… No le están saliendo bien las cosas a los ojos de sus inversores… Los errores se pagan, y los que han pagado ya el pato son sus accionistas:

Sí, a los bancos, en general, les va muy bien que salgamos de rendimientos negativos, pero tienen muchos bonos y les debe estar escociendo en sus cuentas de resultados, los mustios que están recibiendo en bonos…

PD2: Cuando se empieza un trabajo hay que acabarlo. Puede que te lleve muchos días y que cueste mucho esfuerzo. Incluso diría yo, hasta es mejor acabarlo aunque quede mal, que dejarlo inconcluso. Sí, no se pueden dejar las cosas a medias. Además, si ofrecemos el trabajo que hacemos cada día, ¿qué nos diría el Señor, si viera que nos hemos cansado y se lo dejamos a medias? No, hay que terminarlo y, por supuesto, tratar de hacerlo lo mejor que podamos.