Ayer hubo un severo castigo al

que faltaba por caer, el Nasdaq, los valores tecnológicos, las FAANG (Facebook,

Apple, Amazon, Netflix y Google). Llevaban un recorrido endiablado fruto de ser

las inversiones de moda en los últimos años. Les queda recorrido a la baja y

esperemos que no afecte más al resto de mercados que ya habían recortado antes.

Interesantes previsiones:

2018 4Q Economic Capital Market Outlook

If you have been invested in the U.S.

equity markets over the past five years, you have experienced a solid return

and resurgence in the market value of your investment portfolio. In its basic

form, a capital market, is simply a mechanism for pricing risk. Over the past

five years, we have seen increases in prices on publicly traded risk assets,

such as stocks and high yield bonds. However, markets are not necessarily

efficient at pricing risk all of the time. Equity investors have been richly

rewarded over the past five years in spite of growing global risks. However, this period of rising

equity prices and low levels of volatility is about to be tested as the global

economy transitions and capital markets adjust to higher interest rates. The

risk premium, which investor’s demand on risk assets, needs to adjust higher.

The

U.S. economy is performing extremely well and remains one of the stronger

pillars in the global economy. The unemployment rate is near record lows, wage

inflation is taking root, and consumer confidence is high. In addition, excess

resources that have persisted in the economy for many years are being put to

use as capacity utilization improves and occupancy rates in real estate

increase. We are even starting to see improvements in productivity gains that

have been illusive throughout this period of economic growth.

{kind=link}

After

working through the Financial Crisis and slow economic growth that followed, we

believe an inflection point is near. The Financial Crisis required massive

Federal Reserve intervention, such as regulatory bank reform and quantitative

easing, resulting in distorted economic and capital market activity. We are now

experiencing an economic period unlike any other in history. This is evidenced

by a zero percent real Fed Funds Rate and $4.2 trillion in debt on the Fed’s

balance sheet, which it had purchased in the open market. As a result,

comparisons to past recoveries provide little guidance. So, within our

investment matrix, we continue to cling to those things we are clear on:

1.When money supply grows, prices of financial assets

rise.

2.When central banks reduce interest rates to low levels

and keep them there for a long time, asset prices increase.

3.When monetary policy shifts tighter, volatility

increases and markets inevitably dislocate.

4.The credit cycle still exists.

It

is important to separate the corresponding impact of the cumulative regulatory,

political and central bank decisions on the economy from its impact on the

capital markets.

The Economy

The

U.S. economy is in the sweet spot, and we estimate current growth of around 3.0%

as both the business and consumer sectors continue to show resilient strength

this year. The continued improvement in job growth and employment is

contributing to increased consumer strength, which in turn, supports growth in

Retail Sales evidenced by a 5.3% increase over the summer. We expect the

economy to show continued strength through the first half of 2019, and we

predict it will begin to slow in the second half as the impact of higher

interest rates takes effect. With stronger aggregate demand, the risk of a

higher pace of inflation is real, as supply of labor tightens and raw material

prices ratchet higher. The consumer, construction and energy sectors are

showing solid growth. However, declines in auto sales and housing are early

signs of the potential shift in economic activity.

While

the domestic economy is humming along, capital market activity is giving us

some heart burn. When we talk about the capital markets, we include publicly

traded stocks and bonds, as well as other investable asset classes, such as

leveraged loans, real estate, and private equity. The transition from prolonged low

levels of interest rates to a higher interest rate environment will inevitably

cause dislocations in asset prices. Higher interest rates result in

lower valuations. This happens as discount rates adjust higher on private

equity transactions, the risk free rate moves higher when valuing private

investments, and cap rates move higher when valuing real estate investments.

Monetary Policy

Even

though the Federal Reserve is two years into its tightening cycle, monetary

policy still feels accommodative. The

Fed has pushed short term interest rates higher eight times over the past two

years and the Fed Funds rate is now at the same level it was at leading up to

the Financial Crisis in 2008. However, the tightening cycle includes more than

simply adjusting short term interest rates higher. The velocity of money and

private credit expansion have been impediments to the acceleration of growth

over the past ten years.

{kind=link}

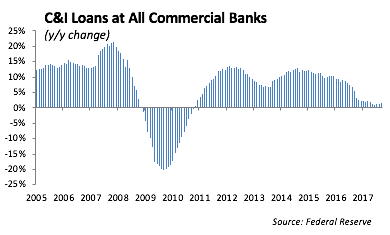

Business

formation and economic growth has also been muted by the abysmal rate of loan

growth from the banking sector. Growth in C&I loans over the past two years

has been particularly weak. As a result, risk has been pushed from the banking

sector into the private markets, where more lending now occurs. When the credit

cycle turns down, the private investors will feel the brunt of it.

Based

on the strength in the domestic economy, we expect the Federal Reserve will

raise rates another 25 basis points in December. However, with Brexit on the

horizon, we expect there to be a global pause in monetary tightening to allow

for sufficient liquidity in the global markets. In addition, we expect the Fed

to begin talking about “a pause” in its rate hike program as uncertainty in the

economic growth begins to form in 2019.

International and Emerging Markets

At

some point, we expect the market will no longer ignore the growing risks

weaving through the global capital markets. These risks include a collapse in

emerging market economies such as Brazil, Turkey and Argentina, the growing

trade war with China, a huge debt growth in global developed economies

supporting spending and economic growth, the ill-fated exit of Great Britain

from the European Union, and the growing populist movement throughout Europe.

We

have always pointed to Italy as the growing problem for Europe. Following the

European financial crisis, Italy did not fully implement the austerity measures

it promised. The Italian government kept spending, and through its budget

deficits, the country has become the fourth largest public bond market. Last

week, with its huge debt burden, weak banking system, and unwillingness to

reign in its fiscal spending, Italy’s new government delivered the

irresponsible budget we had expected. The populist movement wants lower taxes and higher spending on

social programs, which the country can’t afford. Trouble will come once the European

Central Bank stops its quantitative easing program, which includes purchasing

Italy’s debt. At

3.50%, the yield on 10 year Italian bonds is only 30 basis points away from the

yield on 10 year U.S. Treasury bonds!

China

is another major risk for investors. This

risk has more to do with shifting U.S. policy toward China, which was

underscored in an important speech that Vice President Mike Pence gave at the

Hudson Institute last week. Reminiscent of Ronald Reagan, Vice

President Pence bluntly accused China of abusing its economic power, bullying

American companies and stealing their intellectual property. With the exception

of the tariffs imposed on China, we believe the majority of tariff initiatives

will be short lived and illustrate a strategy to renegotiate trade

relationships with strong partners in a manner that, at the margin, better

serves U. S. Companies. However,

we do not expect trade with China to be a simple matter of settling on tariffs

for exports and imports.

Vice

President Pence’s speech reveals a much broader agenda toward China, which

addressed China’s stealing of intellectual property for its own technological

gain, its growing military and reach into the South China Sea, and its position

within the global economy. The resolution of these issues will be long and

arduous, and the tariffs on Chinese goods may persist for a long period

depending on how the administration develops its agenda. While President Trump has

demonstrated his preference to get issues resolved quickly, the resetting of

U.S. – China relations and foreign policy will go on for many years. We expect

the uncertainty of U.S. policy and the disrupting impact of domestic supply

chains to weigh heavily on domestic markets. We believe that

U.S. policy is designed to hurt China’s already weak economy, which is showing

slowing growth and an increase in problem loans. Last week, China reported an

increase in the equivalent of $174 billion in liquidity into its capital

markets. A sustained enforcement of tariffs, which now total over $250 billion,

will have a negative impact on China’s economy.

Get Ready Because Trouble is Coming

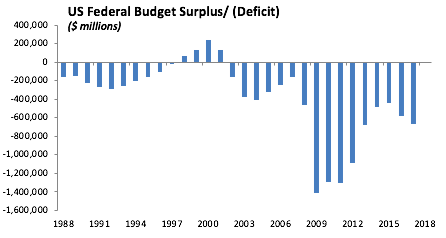

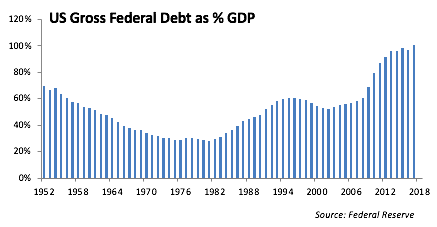

There’s

no other way to say it - the financial position of the United States is a

disaster. After the Financial Crisis in 2008, the

government went on a spending spree designed to stimulate economic growth. As a

result, the U.S. has run budget deficits every year since 2001. The current

budget deficit is projected to reach $650 billion in 2018. The total debt as a

percent of Gross Domestic Product is now at 100%, a level not seen since the

end of World War II.

We

have benefited from nine years of ultra-low interest rates, which have helped

to inflate asset prices. It worked. Now, as the Fed pushes short term interest

rates higher, we expect asset prices should decline. A sustained shift higher in short term interest rates

will most likely lead to increased volatility and some dislocation in equity

markets.

{kind=link}

Investors

are used to being spoon fed by the Federal Reserve, and the financial press

leads investors to believe that this low interest rate environment and record

setting stock market will continue. In a recent interview with Bloomberg,

Federal Reserve Chairman Powell even commented: “there is no reason to think

this cycle can’t continue for quite some time, effectively indefinitely.”

We

are always looking for indications of excesses in capital markets. We view the

strong growth over the past 5 years in real estate development, leveraged

loans, and high yield debt as three signs of excess developing in the domestic

capital markets. In addition, the decline in the quality of loan covenants in

leveraged loan transactions is a concern, and generally, it is presage of a

decline in valuations.

{kind=link}

Prudence

would dictate reducing risk in portfolios given the shift in monetary policy

toward higher domestic interest rates. Interest sensitive sectors, such as autos and

home builders, are having a rough year with Ford and General Motors stocks down

16.6% and 22.7% over the past twelve months respectively. The dichotomy in

performance between stocks in the “old economy” and “new economy” is

significant and continues to warp the structure and performance of Index and

Exchange Traded Funds. Ultimately, we believe we are moving into a period that

will benefit the “stock pickers” approach to managing portfolios.

At

the end of the day, valuation matters for investors. The “Follow the Herd”

strategy and late stage market aggressiveness is more often an ill-fated and

dangerous strategy.

While it is impossible to predict the timing, here’s

what to expect in the near future:

Central bank balance sheets will continue

to shrink, which will put additional pressure on interest rates to rise.

Credit quality will deteriorate as

corporate balance sheets show higher leverage. Expect more downgrades

than upgrades from the rating agencies.

As the credit cycle begins to turn, we

expect an increase in debt restructuring and bankruptcies.

Stock buy backs will continue and take

priority over capital investment.

Volatility will increase as capital

markets adjust to higher interest rates.

The pace of earnings growth in 2019 will

begin to slow, as year-over-year comparisons become tougher after the initial impact

of Tax Reform on earnings subsides.

With higher capital levels and relatively

solid loan portfolios, U.S. banks will weather market turbulence well.

Corporate reorganizations will increase in

late 2019, resulting in a rise in bulk layoffs.

Expected returns in financial assets will

be lower than normalized historic returns.

Abrazos,

PD1: ''El perdón es una

decisión, no un sentimiento, porque cuando perdonamos no sentimos más la

ofensa, no sentimos más rencor. Perdona, que perdonando tendrás en paz tu alma

y la tendrá el que te ofendió'', Santa Teresa de Calcuta.

Todos los días tenemos que

perdonar a alguien, por tonterías, por pequeñas ofensas que nos hacen. Y mira

que cada vez que rezamos un Padrenuestro lo decimos: “…como nosotros perdonamos

a los que nos ofenden…”. Por eso el Señor cuando nos dijo cómo rezar hablo de

esto y no de otras cosas…